In the middle of 2005, we sent to those of you who were with us an 8-page letter (“Irrational Exuberance Moves Home”) describing our analysis that the U.S. housing market was entering a bubble and detailing how its eventual bursting would wreak extreme and widespread economic havoc. Home prices peaked by the middle of 2006 and then began a descent which brought the global economy to the brink of depression.

During the last few months, we have seen signs that the recent mania for houses may have peaked and very recently begun a reversal. It is important that any buyer today be alert to the potential dangers ahead because while the prior housing bubble of the mid-2000s and this current one are not identical, they certainly rhyme.

After the last bubble burst in 2008 home prices fell for a few years and then began to rise again starting around 2012. In the last two years, the pace of price increases quickened. American homebuyers were flush with cash, stock and bond prices were high, and prices for questionable speculations like cryptocurrencies and NFTs exploded to the upside. Surging prices for various assets provided ample funds for mortgage down payments in 2020 and 2021.

Index of U.S. House Prices: Bubbles Then and Now

The long run annualized appreciation rate for homes in the U.S. is little more than 4%. Roughly three-fourths of this figure is caused by general inflation and the other quarter is a combination of maintenance and upkeep costs associated with home ownership plus appreciation above the overall rate of inflation. At the peak of the last housing bubble, home prices were roughly 35% above their long run trend (trend defined by where they would be priced had they continued to rise at their historical rate). Recent prices are 45% above their long-term trend. Home prices after the last bubble fell by 27% on average nationally and to a level slightly below long-term trend. To get back to trend this time, prices would need to decline by 31%.

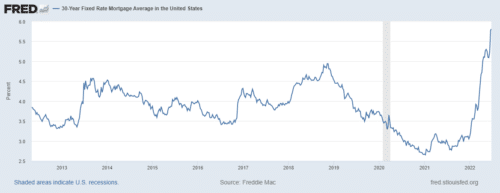

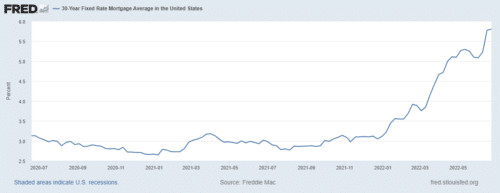

Home prices are greatly affected by borrowing costs. Mortgage rates began the year below 3% and recently hovered around 6%. Never before have mortgage rates doubled in this short a period of time.

Ten Years of Mortgage Rates: Never a Spike Like This

Mortgage Rates Have Nearly Doubled This Year

The steep rise in borrowing costs is making the purchase of a home far more expensive. Consider a home that cost $1,000,000 on January 1st of this year. A buyer of that home with a down payment of 20% ($200,000) and a 30-year fixed mortgage with a rate of 2.95% would carry a monthly mortgage payment of $3,350. A similarly-priced house today brings with it a 5.85% 30-year fixed rate. That causes the monthly payment to soar to more than $4,700. This is a greater than 40% increase for what is usually an individual’s or family’s largest monthly expense. Monthly mortgage costs are more than 100% higher if we consider home prices from January 2021.

When a buyer purchases a home, the buyer’s budget is usually determined by how much can be spent each month on their mortgage. With today’s higher mortgage rates, and building upon the above example, for the monthly mortgage to remain $3,350 as it was at the beginning of the year, the price of the home would need to decline by more than 25%.

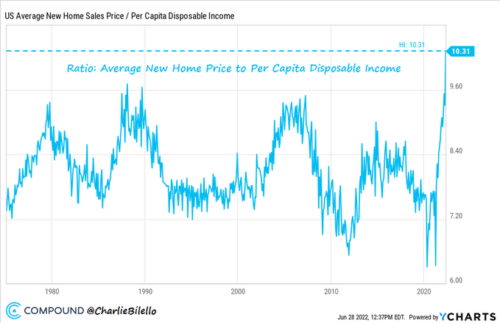

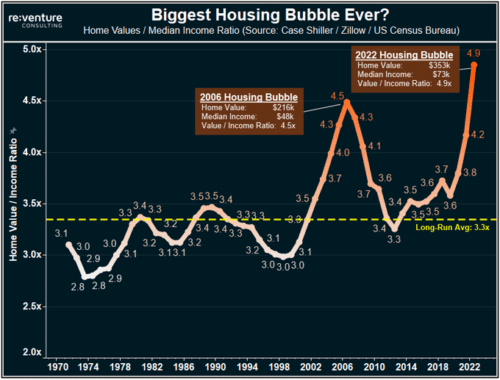

The average price of a home in the U.S. compared to the average level of disposable income: the higher the ratio, the more income that is needed to purchase a home.

Median Home Price Compared to Median Income in the U.S. Sets Record High

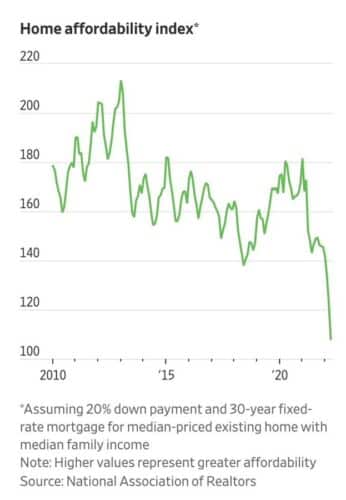

As such, housing affordability is dramatically lower.

Plunging Affordability

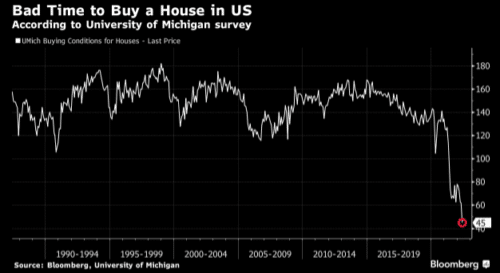

The University of Michigan, known in our field for several valuable economic surveys, produces data that it calls Buying Conditions for Houses. This includes factors such as home prices, mortgage rates, and marketplace sentiment. It is currently plumbing unprecedented depths.

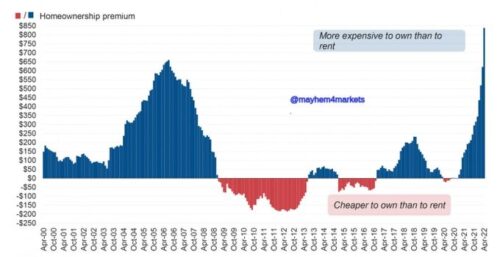

With home prices and mortgage rates elevated, from a purely financial perspective, buying a home is suddenly far less attractive than renting. This disparity recently became more extreme than it was at the peak of the last housing bubble in 2006-2007.

Purchasing a Home Never More Expensive Compared to Renting

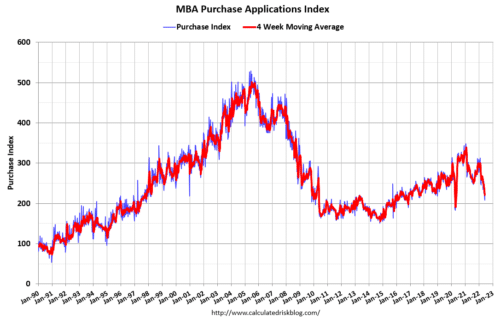

Due to the confluence of higher home prices, steeper mortgage rates, and lower asset prices from which to generate a down payment, home buying activity is slowing. See the decline in home purchase applications depicted on the far right of the graph below.

The decrease in purchasing activity (despite a bump in June at the beginning of the summer selling season) is changing pricing and bidding behavior in the housing market. Whereas until just two or three months ago, sellers were often inundated with bids at elevated prices, today’s sellers are beginning to use price cuts as one way to increase buyer demand.

As of now the housing bubble has stopped inflating, and its bursting may be upon us. If the seasonal increase in selling activity occurs again this summer, it may provide considerable data on the market’s direction by the fall.

The interest rate setting actions of the Federal Reserve will continue to help determine price levels for houses. With inflation at 40-plus year highs, the U.S. central bank is (finally) hiking interest rates. How far the Fed pushes up interest rates is unknowable, but we believe there is a point at which falling asset prices, including stocks, bonds, and houses, will begin to concern those who set interest rates. And, as they have in the past, at that point members of the Fed will then pivot from their current rate hiking program potentially to one of lowering rates again.

The Fed needs to be sensitive to the health of the housing market because housing and housing-related economic activity account for between 15% and 18% of U.S. GDP. If the Fed reverses course from hiking to lowering interest rates, it is possible that housing prices may stabilize and even begin to rise again. But lowering interest rates is not a guaranteed panacea for falling home prices. Currently, for example, sales of homes in China are lower by 42% in the past year despite a decline in both mortgage rates and lending standards. Following the 2006-07 housing bubble bursting in the U.S., rates were lower for a few years before home prices rose again.

The U.S. economy today may be flirting with recession. Potential increases in unemployment, a reduction in the average individual’s savings rate, the inability to tap into alternative assets (particularly in the wake of the crash in cryptocurrencies), among others – if they occur alongside an economic downturn – are likely to play a role in decreasing demand for housing even if rates were to decline.

Fortunately, the lessons of the last bubble were learned by financial institutions in the U.S. Near-death experiences are hard to forget. The housing crash and new regulations successfully purged predatory lending from the marketplace, and much stronger balance sheets are the norm in our country’s biggest banks. Homebuyers the past few years have assumed far less debt and, generally, are not employing the same toxic mortgages that helped fuel the run-up in home prices last time.

Unlike the experience of the last bubble bursting in 2008, we are not concerned about a housing-induced contagion that causes a worldwide near-depression. And, as we concluded in that 2005 letter, for those who purchased a home recently or need to buy now, if the cost easily fits within one’s budget, the buyer should be fine – provided they can look past what might be a turbulent near- to intermediate-term future for home prices. The next few years could look very different for the housing market. So, for those in the U.S. interested in purchasing a home today, we say caveat emptor.