— Paul Volcker“Credibility is an enormous asset.

Once earned, it must not be frittered away.”

In this Issue:

- Celebrating Cheviot’s 35th Anniversary

- Paul Volcker: America’s Great Unsung Hero

- About Cheviot

- Credits and Disclosures

CELEBRATING CHEVIOT’S 35th ANNIVERSARY

Fred Marks began his professional career in the 1960s as an attorney specializing in business transactions, retirement planning, and estate planning. As one of his many intellectual pursuits, he studied investing and eventually was introduced to the concepts of famous investors, including Benjamin Graham and his most well-known student, Warren Buffett. And, as Fred carried on in the legal profession, he witnessed far too often that his clients would suffer investment losses either at the hands of careless investors or by those perpetuating nefarious schemes. Fred knew there was a better way.

In 1985, for less than a $3 ticket, one could see hit movies Back to the Future and Beverly Hills Cop while listening to “We Are the World” on the car ride to the theater. Interest rates in the United States averaged 8%, the world’s population had yet to breach five billion, and Coca-Cola introduced New Coke to great publicity – and even greater confusion. All the while, a handful of Fred’s legal clients were independently trying to convince him to assume the management of their investments. And so that year, after some persuading, Fred began to professionally manage the investments of six legal clients.

Fred’s motivation for beginning his investment firm was to provide safe, long-term growth of the investments entrusted to him. He knew that by keeping his clients out of harm’s way, he would help them reach their financial goals while also providing peace of mind throughout the journey.

One early and enduring component of his investment philosophy was to “win by not losing.” Once firmly established, Fred renamed his company Cheviot Value Management for the neighborhood within Los Angeles in which he lived (Cheviot Hills) and the type of investing espoused by Benjamin Graham and Warren Buffett.

The goals for Cheviot were and continue to be: invest safely to generate long-term portfolio growth with much less volatility than is produced by the overall stock market and provide expert financial planning services – both of which should succeed in helping our clients sleep well at night. Cheviot’s philosophy is always to focus on the long run and ignore short-term fluctuations other than to benefit from them by buying what we deem cheaply priced securities and selling richly priced ones. In order to accomplish this, we at Cheviot think independently, unafraid to disregard the current sentiment of the crowd. It is important to invest patiently, remembering Buffett’s observation that, “The stock market is a device for transferring money from the impatient to the patient.” And, borrowing lessons from Buffett’s long-time business partner, Charlie Munger, we seek to understand the many psychological pitfalls that handicap investors, trying at all times to avoid them, and having the gumption to purchase investments in difficult times and to make sales when all appears cheery.

Often, we are buyers of stocks when they are least liked and media headlines portray a business fallen on hard times. A segment on financial television in which our own Darren Pollock was interviewed was titled, “Why Darren Pollock Loves Stocks You Hate.” And would you believe that the companies at the time that were so truly out of favor that they were considered “hated” were high-quality behemoths like Berkshire Hathaway, Microsoft, and WalMart? Such is the cyclicality and often fickle nature of financial markets. While it may feel uncomfortable in the moment, going against the crowd can be rewarding over time.

Rooted in Cheviot’s desire to keep our clients’ assets safe is the notion that the investments we buy are just as important as those we avoid. Our seeking value in the shares of the companies we purchase helps steer us away from expensive and overly-popular stocks, often fads, that can easily sour on those investors who hold them. The individuals and organizations for which Cheviot works employ us because our investment style grows their wealth over time while also avoiding major market meltdowns. (Of course, past performance is no guarantee of future results. For disclosures, see page 7 of this letter.)

We take great pride in keeping our clients safe during historic periods of tumult. In these pages, Cheviot predicted the 1987 stock market crash just months before it occurred. During the dot com bust years 2000 through 2002, we actually grew our clients’ wealth when U.S. stock prices fell 45%. And Cheviot helped its clients sidestep most of the stock market’s decline during the financial crisis of 2008. True to Cheviot’s founding purpose, we have avoided devastating declines and hope to continue doing so in the future.

Over the years, Cheviot has grown to provide a comprehensive suite of financial services, all of which are included for our clients. We are proud to help clients navigate their way through an often treacherous “financial jungle.”

When asked what makes for an honest member of the financial community, former Federal Reserve Chairman Paul Volcker, considered a paragon of integrity in American finance (and profiled in the pages that follow), replied, “Do they have a fiduciary responsibility or not?” While the term “fiduciary” has a definite legal definition and is adhered to by some though not all firms in our industry, Cheviot always has maintained the fiduciary standard as not just a legal but a moral imperative.

With Cheviot’s growth has come a few small nods of recognition within the industry. Fred never imagined back in 1985 that his quiet firm would eventually be mentioned three dozen times over the past decade in The Wall Street Journal, Barron’s, Bloomberg, and Money Magazine, among others, by some of the most esteemed financial journalists in the business. It is a pleasant surprise every time the phone rings and one of these organizations is on the other end of the line.

For those who visited us when Fred was still involved in the firm’s daily activities, you might recall his desk adorned with several ornamental tortoises. Employing a calm, consistent, and methodical approach, Fred knew, with an assist from Aesop, that slow and steady wins the race. It is one of many beliefs ingrained in Cheviot’s culture. (And speaking of slow and steady, Cheviot’s two principals, Darren Pollock and David Horvitz, have been with the firm for 22 years and 14 years, respectively.)

We thank you, our valued clients, for these first 35 years. And we continue to dedicate ourselves to providing you with the highest standard of personalized wealth management during the next 35 years.

PAUL VOLCKER:

AMERICA’S GREAT UNSUNG HERO

Lessons in Short-Term Pain for Long-Term Gain

Paul Volcker was a superhero of public service and modern finance.

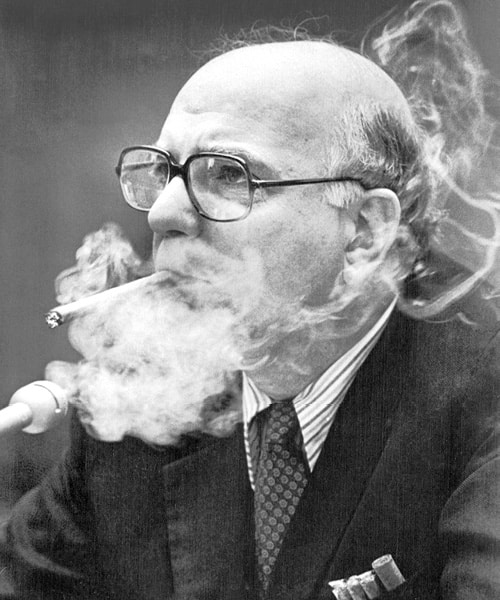

The financial wizard enjoyed cheap cigars, and brought plenty, while speaking on Capitol Hill.

When, in 1971, the U.S. abruptly severed ties between the dollar and gold (preventing holders of dollars from trading them to the U.S. Treasury in exchange for the U.S. government’s physical gold), Volcker was asked to help effectuate the separation. When the U.S. economy suffered from debilitating and seemingly endless inflation, Volcker was asked to fix the problem. When it was discovered that Swiss banks were hiding money stolen from victims of the Holocaust, that the United Nations’ oil-for-food program went awry in Iraq, and that corruption tore through the World Bank, Volcker was asked to fix those complicated problems.

And when the U.S. and global economy crashed in 2008, Volcker, then in his 80s, was asked to craft regulation to help prevent a similar banking crisis in the future. Then, through the Volcker Alliance, to which he donated nearly all of his net worth, Volcker spent his later years trying to improve the effectiveness of civil service by educating and developing current and future members of U.S. government at all levels. Always economical, the 6-foot-7 legend of finance regularly rode the bus to his Rockefeller Center office into his 90s. Paul Volcker died this past December at the age of 92.

25 year-old “Tall Paul” joined the Federal Reserve in 1952. A couple of private sector banking jobs followed before Volcker took a pay cut to return to government in 1962 at the Treasury department. In 1975, Paul was appointed President of the New York Federal Reserve Bank. Four years later, he accepted another pay cut – this time by half – to earn $57,000 as the Chairman of the Federal Reserve, stewarding the monetary system of the U.S. while renting a one-bedroom apartment in a building housing mostly college students.

Offers were made to three others to be Fed Chairman and all three were declined, so difficult was the imminent task of taming runaway inflation that threatened the future of the U.S. economy. Americans, along with markets here and abroad, were losing faith in the government’s ability to resurrect price stability throughout society. Within two months of accepting the job, Volcker made it clear that he would fight inflation not just with words but actions, unexpectedly raising interest rates on a Saturday evening in October. Such drastic action is unimaginable today. Volcker then caused interest rates to briefly reach 22% (today they are closer to 2%), forced the economy into a severe recession, and – in doing so during an election year – vastly reduced then-President Jimmy Carter’s chances for re-election.

He described his momentous accomplishment in a 2019 interview:

“People today may not remember the atmosphere that was experienced. The inflation rate had gone up for more than a decade, there were only feeble efforts to deal with it. During the Ford Administration they handed out Whip Inflation Now buttons. But they had more buttons than policy!”

In 1979, “President Carter asked me to become Chairman of the Fed. It was obvious that existing policies weren’t working. I was already in the Federal Reserve system, voting against some of those policies. I decided we needed a change in our approach and we needed to stop worrying about increasing unemployment and we needed to deal with inflation otherwise it would get worse because it was actually accelerating as it got close to a 15% annual rate. It was going to be 20%. People were really fearful about the stability of the country.

“I saw no other way to approach this other than a bulldog biting at it. And I became plenty worried in 1982 when we did start to get higher unemployment and the damn inflation rate wasn’t coming down. But I felt like we were stuck. We couldn’t back out or all of the effort we were making would be for naught. Fortunately, by the summer of 1982 the money supply came down, the inflation rate came down, we had a recession but by the end of the year it looked like the recession would soon be over or at least not get any worse. It ended pretty quickly. It took that last year of sticking with it that was necessary to do the job.”

Volcker received unyielding criticism for pushing the economy into the worst recession since the Depression of the 1930s. “You talk about how unpopular it was: the farmers had tractors parked outside of the Federal Reserve, we had community groups [organizing against us], one congressman every day for two years called for my impeachment! But my sense was that the country as a whole understood that inflation was grabbing us by the throat and the country understood I was attacking a problem that needed to be attacked.”

From his recent memoir, Keeping At It, he adds, “Did I realize at the time how high interest rates might go before we could claim success? No. From today’s vantage point, was there a better path? Not to my knowledge—not then or now.”

Says investor and Volcker friend, Ray Dalio: “People [today] don’t have any understanding of how challenging that time was. We think of [the financial crisis of] 2008 but in 1982 the unemployment rate rising to 10%, the rate at which the economy plunged was worse than in 2008. It was a more dramatic time.” Volcker’s courage to not abandon the fight against inflation despite political pressures to relent helped save the U.S. economic system as we know it. Dalio continues, “[He] had great wisdom, humility, and classic heroism in which he sacrificed his well-being for the well-being of others.”

Federal Reserve leadership since Volcker left office in 1987 has enjoyed the lack of severe inflation that prevailed during the beginning of Volcker’s tenure. And in sharp contrast to Volcker’s dogged tenacity and capacity to suffer in the short-term for the benefit of the long-term, Fed leaders repeatedly have capitulated to the whims of financial markets for the last 30-plus years. Speaking before Volcker’s passing, bond investor Jeff Gundlach had this to say, “You have to go all the way back to Volcker to see a Fed Chairman who was indifferent to the message of the market and was really driving the market instead of being driven by the market.” The Fed Chairs since Volcker – Alan Greenspan, Ben Bernanke, Janet Yellen, and now Jay Powell – all share the same near-panicked response whenever stock prices decline (a normal function of the financial system) as they continually try to buoy financial markets.

Keeping interest rates persistently low is one way to try to elevate market prices, and over time the Fed has become very creative in its reasoning for why it must keep rates so low. Chairs Bernanke, Yellen, and Powell all targeted an inflation rate of 2% and in some years achieved a lower figure. Today, the Fed says it will not balk at future inflation rising above 2% so long as it makes up for prior years when inflation was lower. When asked a few years ago about the Fed’s provoking higher inflation, Volcker stated bluntly, “Good luck in that. All experience demonstrates that inflation, when fairly and deliberately started, is hard to control and reverse.” He would know. “The real question about loose monetary policy [that which could spur inflation] is: can you reverse it in time? That is always the biggest problem in central banking.”

After Volcker’s passing, former President Carter, whose re-election chances were dashed by the very recession Volcker needed to cause to beat inflation, had this to say, “[Volcker’s] economic acumen made him a giant of public service. Paul was as stubborn as he was tall, and although some of his policies as Fed Chairman were politically costly, they were the right thing to do.”

As a civil servant, Volcker always was driven to do the right thing – even if his actions were unpopular. In his memoir, he wrote, “We have learned time and again that years of financial stability and economic growth tend to involve easing of regulations and supervisory discipline. We see that at work as I write in 2018, with pleas for reduced capital standards for banks.” Volcker makes his own plea: “Can we learn to do better?”

Volcker was distressed by the level of decision making in government today and, through his Volcker Alliance, set out to improve the quality of governance in the U.S. “How do we train people to oversee all that outsourcing [by the U.S. government]? There are hundreds of billions of dollars being outsourced: who’s minding the store? Are people equipped to do that? Have we taught them the right things? Have we taught them how to manage? This little Volcker Alliance is trying to create a marriage between universities and the state and local as well as federal government to see if we can develop a stronger sense of interest and efficiency [in these areas].

“I’d like to see my legacy as a more effective government in general… I would like to see a general acceptance of the need for an efficient public service ethic and to keep people attracted toward public service because they can take satisfaction that they’re doing something concrete for the country… I would like to see that kind of spirit permeate a wider population. And it once did. When I got out of college going into government was a popular thing to do. Now they scratch their head and say why would you ever want to do that? That’s not a very healthy sign. And it goes along with today’s low 20% confidence in government to do things right… Being skeptical is one thing but being anti-government is another. We need to repair it. We don’t dismiss it.

“I’m with Alexander Hamilton,” says Volcker of his political hero. “The true test of government is the ability to get something done efficiently. We lack in that respect.”

Often serving to allay Volcker’s skepticism of the strength of the U.S. government is something his mother would say to him. “Her response, to me, remains the only convincing answer: ‘The United States is the oldest and strongest democracy in the history of the world. In two hundred years it has survived a lot. Now get back to work.’”

ABOUT CHEVIOT

Today, Cheviot Value Management is one of the oldest independent investment advisors in Los Angeles. Its founder, Frederic G. Marks, was an experienced business attorney with a bird’s eye view of the struggles his clients faced when investing their hard-earned savings. Repeatedly, he witnessed his clients incurring losses or being mistreated – sometimes without knowing it – by financial services professionals. Since its founding in 1985, Cheviot’s mission is to provide financial peace of mind through careful investing and thoughtful financial advice. Unlike what Fred witnessed elsewhere in the financial services industry for so many years, his goal for Cheviot was to put the interest of the client ahead of all else. Just be helpful.

We begin, in Fred’s words, by helping clients avoid “uninformed speculation under the guise of investment.” Based on the teachings of legendary investors Benjamin Graham, his most famous student Warren Buffett, and his business partner, Charles Munger, Cheviot seeks to own high quality investments for its clients (and members of the firm right alongside them). Our approach aims to produce a more stable growth trajectory, with less volatility than occurs in the stock market. This helps our investors sleep well at night and enjoy greater long-term success.

Cheviot’s Purpose:

We give our clients peace of mind through safety-first investing, long-term growth, and a steady stream of retirement income. Cheviot prides itself on meeting the long-term financial goals established with our clients and on providing attentive and personal service.

Four principles on which Cheviot was founded:

Integrity:

Put the client first in everything we do.

Invest in securities that can be bought or sold quickly and inexpensively.

Flexibility:

There are no lock-up periods; clients may access their funds at all times.

Affordability:

Invest for the long-term, minimizing all costs and taxes.

Why Cheviot?

We have decades of independent and unbiased experience, serving clients since 1985.

We invest for ourselves and our families the same way we invest for our clients: We “eat our own cooking.”

We do not sell any investment “products” nor are we affiliated with any other financial service companies that do. There are no hidden fees.

We have been recognized by the financial industry’s leading publications including, Barron’s, Bloomberg, The Wall Street Journal, Money Magazine, Fox Business, the Business News Network and CNBC.

We maintain well respected credentials in the financial industry, including the Certified Financial Planner (CFP®) designation.

We treat our clients in the way we would desire if our roles were reversed.

CREDITS

Darren C. Pollock, David A. Horvitz, Jim Whiting, and Scott Krisiloff, CFA authored this issue of Investment Values.

DISCLOSURES

Founded in 1985, Cheviot Value Management, LLC specializes in providing investment portfolios with the long-term goals of growth of capital and income production over time. Included within the management of a client’s investments, Cheviot Value Management, LLC also provides financial planning advice including potential strategies related to tax considerations, estate planning, insurance coverages, philanthropy, and next generation preparation. While not a professional tax or legal advisor, Cheviot Value Management, LLC assumes no liability for any tax or legal advice given. Cheviot Value Management, LLC offers such suggestions with the expectation that they will be further examined by a tax or legal professional.