— C. F. Ketterling“My interest is in the future because I’m going to spend the rest of my life there.”

In this Issue:

- Our Investment Outlook

- Presidential Elections and the Stock Market

- Year-End Financial Planning Considerations

- Credits, Disclosures, & Notes

OUR INVESTMENT OUTLOOK

Powerful fiscal stimulus in the wake of the Covid pandemic ended what would otherwise be an ongoing economic depression. Stimulus checks to millions of American citizens helped retail sales remain strong across various industry groups including furniture, consumer electronics, motor vehicles, and more. The eventual handoff from government stimulus to a rebounding economy will be gradual and important. In recent months, consumer confidence rebounded even as the next stimulus package is slow in its formation. Helping buoy consumer sentiment, stock prices rose at a healthy clip in the third quarter to arrive in positive territory for this most unusual year when national incomes aided by relief payments actually rose despite considerable economic damage. On the cusp of cooler weather, we hope the virus will be contained and that effective vaccines will be available in the first half of next year, but we fear higher case counts will lead to a challenging several months. As occurred this past spring, Cheviot will be ready.

The Federal Reserve, by lowering interest rates to zero and gushing liquidity into the financial system, is responsible for higher share prices. It is fair now for experienced investors to grow curious about the side effects from the largesse of the Fed’s ongoing market support. When asked in September if stimulating by more than $100 billion per month and then keeping interest rates very low for several more years might cause inflation in asset prices enough to foment a future bubble, Fed Chairman Jay Powell rejected the premise. Citing a decade of data during the past ten years in which rates were held very low in the wake of the 2008-09 financial crisis, Powell stated that no bubbles were created. We immediately had flashbacks to former Chairman Ben Bernanke stating in the midst of the mid-2000s housing bubble that it did not exist. As long-time clients know, we described in great detail at that time how off the mark that was.

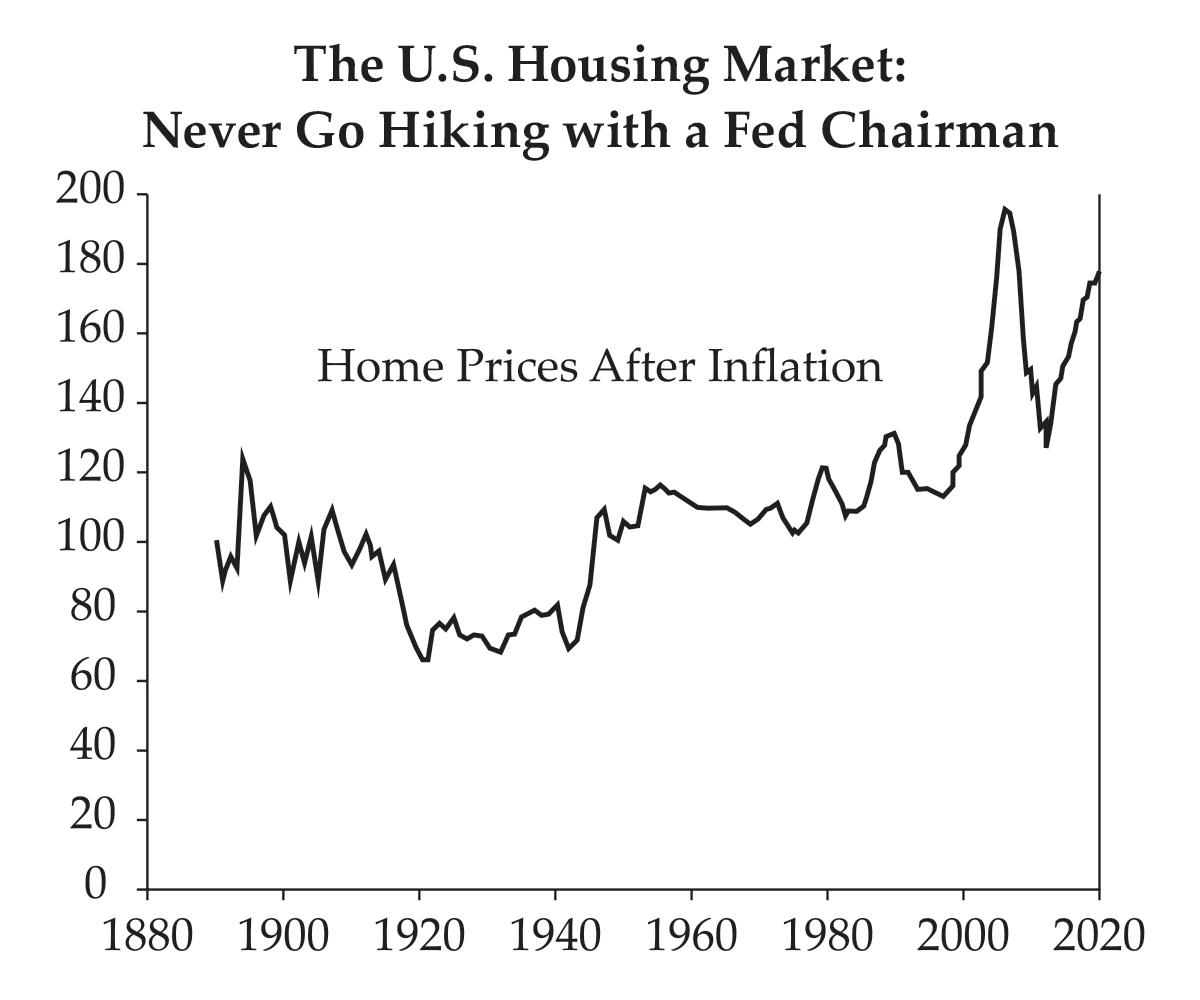

Home prices in the graph below are displayed net of inflation. For 50-plus years, there was zero housing price appreciation above the rate of inflation (this is not widely understood). Then home prices in the U.S. spiked higher in the mid-1940s upon the return of soldiers from WWII as household formation dramatically increased. Subsequent to that one-time jump in home prices, residential real estate prices in the U.S. stagnated (again after accounting for inflation) until two mini-manias in the late 1970s and late 1980s. Then home prices soared into the greatest financial bubble of all time in the early-to-mid 2000s. Mount Everest on the graph is the bubble Bernanke did not see. The neighboring peak to its right is what Powell claims not to see. In addition to the unprecedented level of debt in the economy, the weight of this current real estate mania will force the Fed to keep interest rates low for a very long time.

Then home prices in the U.S. spiked higher in the mid-1940s upon the return of soldiers from WWII as household formation dramatically increased. Subsequent to that one-time jump in home prices, residential real estate prices in the U.S. stagnated (again after accounting for inflation) until two mini-manias in the late 1970s and late 1980s. Then home prices soared into the greatest financial bubble of all time in the early-to-mid 2000s. Mount Everest on the graph is the bubble Bernanke did not see. The neighboring peak to its right is what Powell claims not to see. In addition to the unprecedented level of debt in the economy, the weight of this current real estate mania will force the Fed to keep interest rates low for a very long time.

When interest rates are significantly higher than they are currently, income from low-risk assets like investment-grade bonds, U.S. Government debt, and bank CDs can be sufficient for many investors. Low interest rates, however, and the expectation that rates will remain low for many more years, increase demand for a variety of assets including stocks and real estate. This demand can keep asset valuations at higher-than-average levels for considerable periods of time. And, with the Fed intent on cultivating a bit more inflation than the economy has experienced in recent years, this may cause investors to shift their attention to areas that can better withstand debasement of the world’s major currencies. Berkshire Hathaway made headlines recently when it acquired a stake in one of our favorite gold mining companies. If the Fed succeeds in fostering greater inflation, it may create a landscape for many investors that is different and more challenging than what they have experienced in a long time – if ever before. Although greater inflation is an invisible tax that poses difficulties for society at large, as investors, we very much like our chances in such an environment.

PRESIDENTIAL ELECTIONS AND THE STOCK MARKET

With the upcoming presidential election, it is common to encounter speculation about which candidate or party might boost stock market returns and which could depress them. And we at Cheviot are often asked which candidate or party will provide us with a better or worse stock market reaction. How much should the election impact what we do as investors? Given the current interest in this subject, we review three ways in which stock market performance may – or may not – correlate with the outcome of the presidential election.

First, we consider a pre-election question regularly asked of us: “Which party is better for the stock market?” Then, we examine the phenomenon known as the “election cycle” by which one may be able to generally predict the performance of the stock market according to the year of the presidential term. Finally, we look at the potential correlation between the stock market’s performance in the months leading up to an election and the outcome of that election.

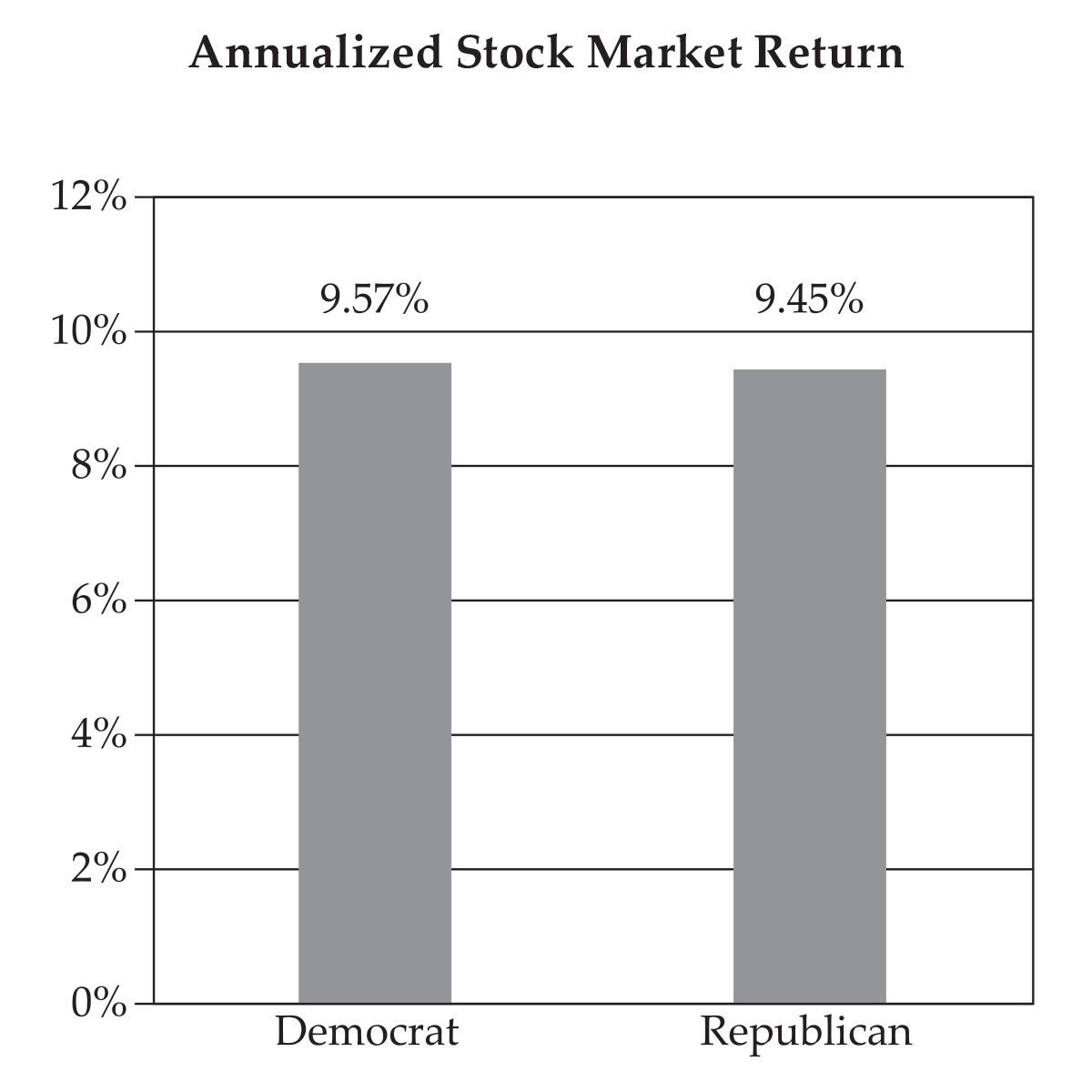

It is often assumed that stock market returns are higher when a Republican president occupies the Oval Office. A common perception is that Republicans are fundamentally pro-business and anti-tax, whereas Democrats are often perceived as anti-business and in favor of raising taxes to redistribute wealth to the lower socioeconomic classes. Perhaps surprisingly, stock market returns since the 1852 election of Franklin Pierce1 and to the 2020 presidential election are very similar regardless of which party is in office. For the nearly 170 years surveyed, stocks returned 9.45% annually with a Republican in office compared to 9.57% per year for Democrats.2

Perhaps this counter-intuitive reality stems from investor pessimism about the future of the economy when it becomes clear that a Democrat will win the presidency. Afterward, investors may cause share prices to rally if they are pleasantly surprised that the economy produced better than anticipated results. Perhaps the stock market rallies on the hope that a Democrat is more likely to increase government spending to stimulate the economy. Possibly, share prices rise ahead of a Republican victory – the market is forward looking and trying to anticipate future economic results – and then share prices may climb less or even fall over time. Despite possessing a pro-business reputation, perhaps the perception – whether true or not – of being more fiscally conservative keeps share prices from rising more than one would intuit during a Republican presidency.

Tying stock market performance exclusively to the party of the president ignores other stronger influences, such as the majority party in Congress over the same periods. Tax legislation originates in the House of Representatives and the composition of this legislative branch appears to be a better predictor of stock market performance than who occupies the White House. The purpose of the Federal Reserve is to attempt to boost or temper economic growth (we know it has been a long time since it has overheated but, recall, when the economy does grow too quickly, the Fed often aims to cool it down). These actions likely carry with them a stronger correlation to the movement of prices on Wall Street than any other government entity. Other factors obviously have a powerful influence over the direction of the stock market including investor perception pertaining to the state of the domestic and global economy, currency fluctuations, business cycles, and the like. Substantive geopolitical events always carry with them the potential to move markets in the short-run (often presenting buying opportunities). Today, the future path of Covid, its impact on the economy and the fiscal and monetary response to that impact will play a significant role in investor appetite for stocks.

Regardless of which party occupies the highest office, an examination of stock market performance as measured by the S&P 500 Index from 1948 through 2019 shows a relatively strong relationship between stock market performance and the election cycle.

The data show that the stock market’s performance, on average, is worst in the first year of a presidency. The market is more likely to reach bottom in the second year than any other presidential year. The third year average performance is the greatest of the four years while the fourth year usually plays host to another strong showing.

With so much focus on the presidential election and the tendency for candidates to sling mud not just at each other but toward the economy (as context for their explanation of how much better they, as president, would manage the economy), it seems counterintuitive that the stock market would typically post strong gains in the fourth year of a presidential term. But there are, in fact, several possible reasons why this is so. In that fourth year it is relatively unusual for large and ground-shaking legislation to emerge from Congress that would impact the economy. It is also less likely for the Federal Reserve to raise interest rates, thus disturb the stock market, during a year four. And often the benefits from stimulus sought by presidents in year three – following the typically weaker stock market and economic periods of years one and two – gain traction in year four.

The fourth year of the president’s term plays host to an average stock market gain of nearly 7% dating back to the onset of (and including) the Great Depression. Since that time, there have been only four election years in which the market suffered a sizable decline. Those years and declines are 1932 (15.1%), 1940 (15.3%), 2000 (9.15%), and 2008 (37.0%). During the two years 2000 and 2008, the market lost a combined 42.8%. During those same years, Cheviot clients enjoyed total gains of 3.3%. (Regrettably for everyone, Cheviot was not yet in business during the years 1932 and 1940!)

Historically, stock market volatility picks up in the month leading up to the election. And it is not unusual for the market to cease trending higher during this time. On average, and with a nod to the marketing department at Coca Cola, this has proven to be the pause that refreshes. Stock prices tend to resume their upward march in the aftermath of the election, perhaps in expression of relief that the mud-slinging of the campaign has ended and/or the increased calm that comes from knowing that little political action will occur in the final couple months of a president’s term. (As Imelda Marcos reportedly said about the post-election period: “Win or lose, we go shopping.”)

There is much consternation that this election may bring with it historical abnormalities. We could witness the first contested election since 2000. Not immediately knowing the outcome of the election is likely to increase financial market volatility in the short run yet have much less impact over the longer term. Should Joe Biden defeat Donald Trump, a less than smooth transition of power could also spur a period of volatility.

During the past four years, the Trump Administration did not adhere to the time-honored techniques of managing the economy according to the election cycle. Immediately after taking office, the Trump Administration ushered in a series of pro-business executive orders and promised significant tax cuts to American businesses and individuals. This boosted U.S. GDP growth to 2.7% in 2017 from 2.1% in 2016. Growth in 2018 slowed just a bit to 2.5% and dipped again to 2.3% in 2019. Even in the absence of Covid the economy may have slowed further in 2020 and the White House would have had little to no ammunition left to give it a boost. Prior to the Trump Administration, U.S. economic growth since 1930 has averaged 2.9% in years one and two, then climbs to 3.8% for years three and four.

Even though the data show a seemingly high correlation between the economy’s and stock market’s performance with the year of the presidency – and though the data may prove to be reliable in the future – we believe the number of periods measured is too short to be significant in a way that should cause investors to change their behavior. Certainly it is something we think investors should not blindly follow. The Trump Administration not following the election cycle is just one reason. And among the world’s best investors throughout the period surveyed (including Warren Buffett, John Templeton, Peter Lynch, and Julian Robertson, to name a few), never has one of them credited the election cycle as reason for their success. Says the great Peter Lynch, “I think people are missing what makes stocks go up. They pay way too much attention to the big things like a Democratic or a Republican president.” It proves far better to pay greater attention to owning strong companies and on not paying too high a price to buy their shares.

While we have focused thus far on how a president’s party or the year of his term may impact stock market returns, we have found that the stock market may actually impact or predict the presidential election. It turns out that the price performance of the S&P 500 Index during the three calendar months leading up to the presidential election has been a good predictor of whether the president or his party would be reelected or replaced. A price rise in the S&P 500 Index from July 31st through October 31st traditionally has predicted the reelection of the incumbent person or party. A price decline during this period has pointed to a replacement. Since 1948, this election prognostication method accurately predicted 92% of the time which party would win the election. Going further back, to 1900, and using the direction of the market during the last 60 days before the election yields an accuracy rate of 95%.

There is a valid reason for why the stock market’s behavior may play a role in determining the next president. It is not that the stock market has any immediate or direct connection to the presidential candidates. It does, however, reflect economic sentiment in the period when undecided voters are determining their presidential preference. Additionally, and in a reflexive way, the stock market can impact the voter’s perception of the economy. For many individuals, it is natural to assume that a rising stock market is the product or reflection of a healthy underlying economy. On the other hand, a declining stock market, often considered a reflection of a poorly performing economy, might give reason for a change of political party in the Oval Office.

While this year certainly feels different – and it may accurately be viewed as an anomaly, the performance of the stock market leading up to the November election may provide the final bit of support for electing the incumbent party or assist in turning voters toward different leadership. Either way, come October 31st the market observer turned presidential election prognosticator may be armed with valuable information that helps make for an educated guess as to who might win the upcoming election.

Regardless of who wins this November, for many more months if not quarters, the Federal Reserve will continue to stimulate financial markets out of fear that interest rates would rise and the economy could suffer without such stimulus. The American economy will further recover from the Covid disruption in an uneven fashion.

As for whomever is elected, we have studied the possible near-term impacts on the U.S. economy and are not too worried about them. (Don’t get us wrong, we have PhD’s in worrying, so we can’t help but be somewhat concerned.) But, the more important longer-term view of the American economy should be little changed. Warren Buffett summarized this idea succinctly at the 2016 Berkshire Hathaway annual meeting: “In my lifetime, GDP per capita in real terms has gone up six for one… I’m confident that 20 years from now there will be far more output per capita than there is now. No presidential candidate or president is going to end that. They can shape it in ways that are good or bad, but they can’t end it.”

YEAR-END FINANCIAL PLANNING CONSIDERATIONS

In addition to investment management, we frequently help our clients with other important areas of their financial lives. These matters include retirement and estate planning, charitable giving, insurance advice, and more. Because we are dedicated to providing personalized financial advice, the below recommendations are broad overviews whose finer points we would be glad to further discuss with you. There are some notable changes to consider as we near year-end. As clients, you are always welcome to contact us with specific financial questions, no matter how big or small.

New Rules for Required Minimum Distributions (RMDs)

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed on December 20, 2019, established some new rules for retirees, particularly regarding annual Required Minimum Distributions (RMDs) from IRA and 401k accounts. If you turned 70½ prior to January 1, 2020, then the old rules apply. For everyone else, the new RMD age is 72, which means you do not have to start taking RMDs from your IRAs, 401(k)s, and other qualified accounts until the year you turn 72 (or as late as April 1st of the following year).

Also note, that due to the economic crisis caused by the Covid pandemic, all RMDs for 2020 are suspended.

No Age Limits on Retirement Contributions

Prior to the passage of the SECURE Act, taxpayers age 70½ or older were prohibited from making contributions to their IRA accounts. As of January 1, 2020, anyone with qualifying income is eligible to make contributions to their IRA or Roth IRA accounts. Individuals may consider making a tax-deductible contribution to your IRA or a non-deductible contribution to your IRA and then converting to a Roth IRA.

Inherited IRAs

The “stretch” or “lifetime” withdrawal schedule has been eliminated for non-spouse beneficiaries of Inherited IRAs inherited after January 1, 2020. The new limit will be within 10 years of the death of the original account holder, but if you started taking RMDs before 2020, you are grandfathered in with the old rules. Again, because of the pandemic, all RMDs, including those from Inherited IRAs, for 2020 are suspended.

Consider Charitable “Bunching”

Because of the Tax Cut Jobs Act, the standard deduction is much higher than it used to be. ($12,400 filing single, $24,800 for married filing jointly). This is a good thing for many people because the sum of their home mortgage interest, charitable giving, state & local taxes, etc. are lower than the standard deduction. Individuals or families whose itemized deductions are close to the standard deduction should consider “bunching” or delaying gifts in 2020, and then doubling up in 2021. That way, they could take advantage of the high standard deduction in 2020 and then push their deductions over the threshold in 2021.

Make Charitable Gifts

Most gifts to qualified charities are tax-deductible. Donating before year-end allows the taxpayer to deduct the donated amount in the year of the gift, provided they do not take the standard deduction when filing their taxes. Rather than donating cash, consider donating securities that have appreciated. By donating shares of highly appreciated stock, for example, the donor receives a deduction in the amount of the full fair market value of the security as of the date of donation. This has the dual benefit of avoiding capital gains tax on the appreciated amount of the investment and preserving cash that would otherwise have been donated. Additionally, the same quantity of shares that were donated could also then be purchased with a new – and tax-friendly, higher – cost basis.

As an alternative to donating directly to a charity or to multiple charities, donors can establish and donate to a Donor-Advised Fund (DAF). This fund acts as a repository for donated assets to be distributed to qualified charities at a later time. The donor receives a tax deduction for the full amount donated to the DAF in the year in which the funds are donated, even if the DAF distributes the funds over a period of years.

Make Annual Gifts to Family Members (or Others)

The 2020 annual gift tax exclusion is $15,000. This gift amount can be given to as many individuals as you like, without reducing your lifetime gift and estate tax exemption. The gift is tax-free to the recipient, and, while not tax-deductible to the donor, the funds reduce the value of donor’s estate and subsequent estate taxes at death. No gift tax return is required to be filed for gifts that do not exceed $15,000.

Make Large Inheritance Gifts During the Next Few Years

The gift/estate exemption base increased in 2020 to $11,580,000 per individual. (Couples can give double that amount since each person can contribute the new maximum). This means that estates can pass assets to heirs without additional estate taxes under the lifetime limit mentioned above. Because this law is in effect until 2025 (at which time the gift/exemption base could revert to a lower number), individuals with very large estates should consider taking advantage of the current law. For such individuals, it may prove wise to transfer some wealth in the next few years in case this tax law becomes less favorable in the future.

Harvest Capital Losses Against Taxable Gains

At Cheviot, we do not advocate allowing taxes to dictate investment strategy. However, we will examine opportunities in the portfolio to offset realized capital gains and the taxes due on them. For example, an investor in the highest tax bracket who sells a stock for a gain within one year of having purchased it will owe roughly 50% of that gain in federal taxes and state taxes. But by selling an equivalent amount of a losing stock, the investor can eradicate the gain and have a resulting tax bill of $0. If capital losses exceed capital gains for the year, up to $3,000 of those realized losses can be used to offset ordinary income (or $1,500 for married taxpayers who file separately). The remainder can be carried forward to offset gains in future years.

Don’t Spend Your HSA Dollars (If You Don’t Have To)

Among the many benefits of a Health Savings Account is that the tax-deductible contributions do not need to be spent before the year’s end. In fact, the money can remain in the account and continue to grow tax-free and be withdrawn tax-free when used for qualified medical expenses. Additionally, there are no required minimum distributions (RMDs) from Heath Savings Accounts. So, if you are able to delay spending the funds, you can secure many years of tax-free compound growth. This can continue throughout life, even while the IRS is forcing accountholders to make withdrawals from their IRAs after 72 years of age. An HSA is perhaps the most tax-advantaged savings tool there is, so – if you are eligible for an HSA – be sure to contribute the maximum amount allowed before the end of 2020.

Refinance Variable Rate Debt

Interest rates are once again at historic lows. Because of this, now is the time to refinance or pay off loans that have a variable rate in danger of rising over time. A fixed rate may be slightly higher than current variable rates, but in the long run, fixed rates today could be substantially lower than variable rates in the future, creating considerable savings in interest costs.

For all Cheviot clients, we are happy to discuss with you any of these and any other financial planning strategies.

ABOUT CHEVIOT

Today, Cheviot Value Management is one of the oldest independent investment advisors in Los Angeles. Its founder, Frederic G. Marks, was an experienced business attorney with a bird’s eye view of the struggles his clients faced when investing their hard-earned savings. Repeatedly, he witnessed his clients incurring losses or being mistreated – sometimes without knowing it – by financial services professionals. Since its founding in 1985, Cheviot’s mission is to provide financial peace of mind through careful investing and thoughtful financial advice. Unlike what Fred witnessed elsewhere in the financial services industry for so many years, his goal for Cheviot was to put the interest of the client ahead of all else. Just be helpful.

We begin, in Fred’s words, by helping clients avoid “uninformed speculation under the guise of investment.” Based on the teachings of legendary investors Benjamin Graham, his most famous student Warren Buffett, and his business partner, Charles Munger, Cheviot seeks to own high quality investments for its clients (and members of the firm right alongside them). Our approach aims to produce a more stable growth trajectory, with less volatility than occurs in the stock market. This helps our investors sleep well at night and enjoy greater long-term success.

Cheviot’s Purpose:

We give our clients peace of mind through safety-first investing, long-term growth, and a steady stream of retirement income. Cheviot prides itself on meeting the long-term financial goals established with our clients and on providing attentive and personal service.

Four principles on which Cheviot was founded:

Integrity:

Put the client first in everything we do.

Invest in securities that can be bought or sold quickly and inexpensively.

Flexibility:

There are no lock-up periods; clients may access their funds at all times.

Affordability:

Invest for the long-term, minimizing all costs and taxes.

Why Cheviot?

We have decades of independent and unbiased experience, serving clients since 1985.

We invest for ourselves and our families the same way we invest for our clients: We “eat our own cooking.”

We do not sell any investment “products” nor are we affiliated with any other financial service companies that do. There are no hidden fees.

We have been recognized by the financial industry’s leading publications including, Barron’s, Bloomberg, The Wall Street Journal, Money Magazine, Fox Business, the Business News Network and CNBC.

We maintain well respected credentials in the financial industry, including the Certified Financial Planner (CFP®) designation.

We treat our clients in the way we would desire if our roles were reversed.

CREDITS

Darren C. Pollock, David A. Horvitz, Jim Whiting, and Scott Krisiloff, CFA authored this issue of Investment Values.

DISCLOSURES

Founded in 1985, Cheviot Value Management, LLC specializes in providing investment portfolios with the long-term goals of growth of capital and income production over time. Included within the management of a client’s investments, Cheviot Value Management, LLC also provides financial planning advice including potential strategies related to tax considerations, estate planning, insurance coverages, philanthropy, and next generation preparation. While not a professional tax or legal advisor, Cheviot Value Management, LLC assumes no liability for any tax or legal advice given. Cheviot Value Management, LLC offers such suggestions with the expectation that they will be further examined by a tax or legal professional.

NOTES

- There’s nothing significant about Pierce or the year 1852. It’s simply that, well over a decade ago when we began our study of the president’s term and possible implications for stock market gains, we believed that surveying well over a century and a half of history was sufficient. ↩

- There are other studies which survey shorter time periods and conclude that one party is more likely than another to preside over a rising stock market. But, from a statistical standpoint, the sample size is more meaningful when more years are included. And, there is the tendency for a greater number of years to cause the results to even out. Evaluating a far different rivalry, for example, if you took any given year or even decade of baseball games played between the Dodgers and Giants, one team could dominate the other. Yet since their first meeting in 1883, and after more than 2,500 games against each other, the two teams are nearly even: 50.4% of victories went the Giants’ way versus 49.6% for the Dodgers. ↩