— Fred Marks“Over time equities [stocks] are safer than bonds and real estate. One just has to know how to deal with the market fluctuation of equities… It has never troubled me when shares of a company tumble – if I like the company.”

In this Issue:

- Our Investment Outlook

- Zooming with Charlie

- Fred Marks: In Loving Memory

- Credits, Disclosures, & Notes

OUR INVESTMENT OUTLOOK

What a year it was.

Entering 2020, nobody foresaw a year in which a novel virus would infect 83 million individuals globally (unofficial counts being much higher) and cause more than 1.8 million deaths (with excess mortality over 2019 depicting a significantly higher toll).

Scientific ingenuity and the pace of medical progress was remarkable with the creation, production and nascent distribution of vaccines aided by emergency use authorization in many developed nations. Governments cooperated with the medical community and pharmaceutical companies – heretofore competitors – cooperated with each other to forge a silver lining for 2020. Developed nation governments the world over also stepped in with massive fiscal support to sustain economies roiled by the spread of the virus and attendant societal shutdowns. Financial markets were a distinct beneficiary of the unprecedented largesse of coordinated governmental monetary response and, as they look past the present and toward the future, stock prices rallied after a historic drop in the year’s first quarter.

Also unprecedented was the bifurcation caused by the seismic shift in the economic landscape. Some industries, nearly one year since the widespread onset of Covid, remain completely shut down whereas others are thriving. Within industries, larger players saw their strengths magnified relative to smaller competitors. One example: many fast food and large chain restaurants gobbled up market share versus their independent brethren. 110,000 – or more than one in six – U.S. small restaurants closed in 2020. Economic disparity widened not just within industries but individuals, too. The global and domestic hunger crisis is worse now than any time in generations, yet speculative and highly questionable investments soared in price.

Some established and household-name companies today carry valuations whose lunacy rivals that of the greatest financial bubble of our lifetime in 1999-2000. In many cases, the shares of companies bought during that bubble are still well underwater at present (more than 20 years later). This multi-decade destruction of value occurred even for businesses that 20 years ago were profitable.

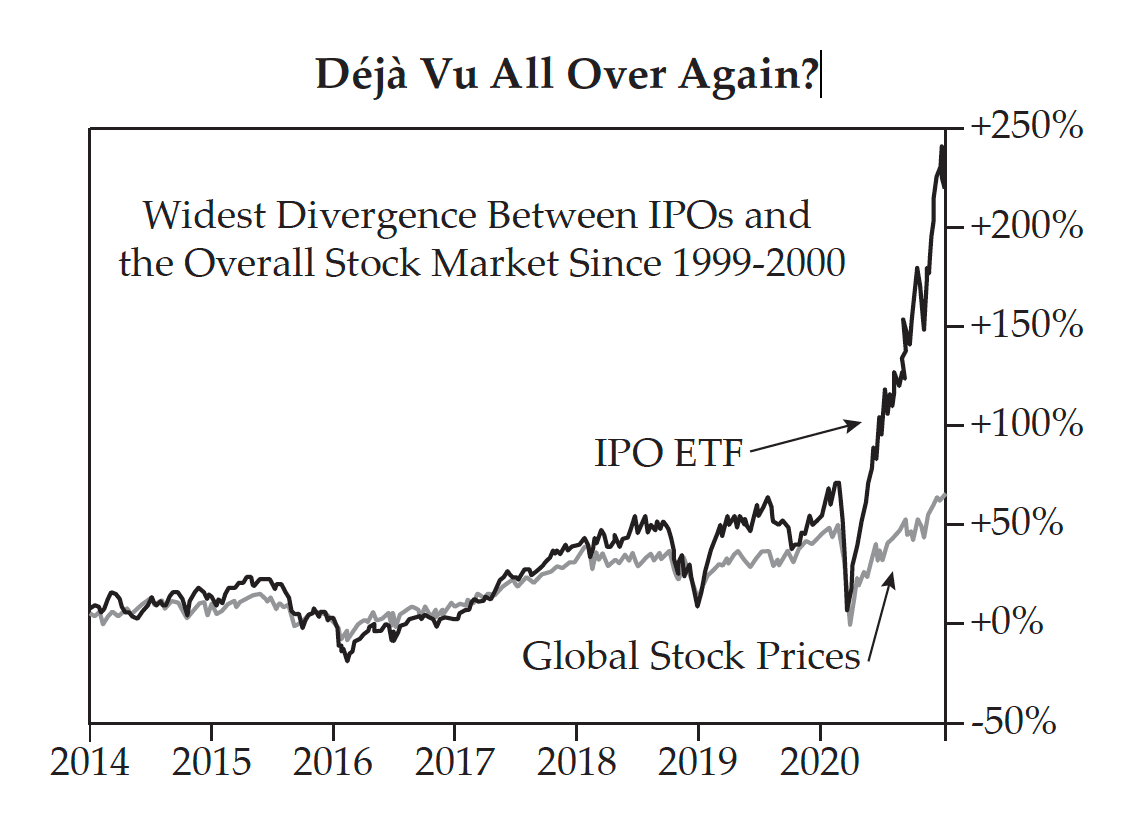

Remembering the initial public offering (“IPO”) party of 1999-2000, one has a sense of déjà vu. The second half of 2020 hosted a wellspring of hot new offerings with successful public launchings that made their private owners and, importantly, sellers very happy. Reflecting their immense popularity, IPOs that went public in 2020 are priced at an average of 24 times revenues (not profits but revenues), a figure exceeded only by the 1999-2000 IPO mania during the biggest tech bubble of all time. By comparison, stocks listed on the tech-heavy and relatively highly-valued Nasdaq trade for an average of four times revenues.

Airbnb, DoorDash, and Snowflake were three of the year’s highlight fliers. Their spectacular debuts were outpaced by other large IPOs merely three times in history – each occurrence by a company that went public in 2000. (One of which was Palm, Inc., maker of the Palm Pilot. Remember those cute, cutting edge Palm Pilots? In April 2000 we wrote in these pages about the absurd valuation, more than $50 billion, market participants granted the company before its stock declined by 97%.)

Because travel was halted for much of 2020, consider figures from 2019 which show that hotel companies Hyatt, Hilton, and Marriott combined for $11.4 billion of revenue and $2.9 billion of profit. That same year, Airbnb grossed $4.8 billion for a net loss of nearly $700 million. Yes, Airbnb is growing much more quickly than the established hotel chains but it is not without competition. And today, when investing experience is valued less than at other times in history (a cycle that will forever recur), to buy all the shares of Airbnb, one would need to pay more than the market values for all the shares of Hilton, Hyatt, and Marriott combined. Given its sky high valuation, Airbnb has some serious growing to do.

The fluctuation of stock prices worldwide and those of IPOs typically move in similar directions. That changed this past spring as many stay-at-home individuals poured their newfound time and money into IPO shares seeking – and by their very demand, effectuating – fast gains. Is this an anomaly or will it be sustainable? See the nearby graph for a price illustration. If history is any guide, those who sold will be glad they did.

There are nearly 75 private U.S. companies founded in the last several years that are valued at more than $5 billion and have yet to come public. Founders and early investors in those companies surely must be interested in selling their shares to the public before the current IPO euphoria fades. While knowing which companies will rise after going public requires a bit of luck, with this many companies on deck, the frothy IPO market is unlikely to soon fizzle.

The economy in 2021 will continue to face the challenge of the slow eradication of Covid but should perform much better than in 2020. Consensus is that the recovery will continue to progress as the year wears on, and we do not disagree. A successful vaccine rollout should unleash pent-up demand throughout various industries as individuals seek to make up for the lost time of the past year. Stock prices, already anticipating such a return to growth, are high and the expectation is that the Federal Reserve will continue to be supportive of the market and economy in many ways combined with significant fiscal stimulus.

As it is a common occurrence, even during economic rebounds, we will not be surprised at some time this year to see considerable fluctuations in stock prices – either across the market as a whole or within specific industries. Such fluctuations will give us opportunities to acquire high-quality businesses at intelligent prices. The capital you entrusted to us is important and we will manage it, with our own personal capital alongside yours, with great care. In the words of Cheviot’s founder Fred Marks, you can count on us to “Always invest. Never speculate.”

ZOOMING WITH CHARLIE

Charlie Munger, Berkshire Hathaway’s Vice Chairman and long-time business partner of Warren Buffett, took to Zoom to be interviewed by a representative from one of his alma maters, Caltech, in mid-December. A genuine polymath whose mental processing power is admired by the likes of Buffett and mutual friend Bill Gates, Charlie is known for providing insightful takes on a wide array of current topics. (For a deeper look into the mind of Munger, see Darren Sits Down with Charlie Munger online, or we can send you the letter upon request.) What follows are a smattering of perspectives shared by the 97 year-old Munger when we attended the aforementioned video conference.

Charlie began by comparing businesses to matters of biology which are born and grow only to recede and perish.

“Over the long term, big companies of America behave more like biology than they do anything else. In biology, all the individuals die and so do all the species. It’s just a question of time. And that’s pretty well what happens in the economy, too. All the things that were really great when I was younger have receded enormously and new things come up and some of them have started to die. That is what the long term investment climate is and it does make it very interesting. Look at what’s died. All the department stores. All the newspapers. U.S. Steel. John D. Rockefeller’s Standard Oil is a pale shadow of its former self. It’s just like biology. They have their little time and then they get clobbered.”

Given the landscape in which businesses evolve, how do investors deal with change?

“Some people try to get on the cutting edge of change so they [try to] destroy other people instead of being destroyed themselves. Those are the Googles and the Apples and so forth. Other people, like me, do some of that – joining things like Apple [through investment] – and in some ways we just try to avoid big change that is likely to hurt us. Berkshire Hathaway, for instance, owns the Burlington Northern Santa Fe Railroad. You can hardly think of a more old-fashioned business than a railroad business. But who is ever going to create another trunk railroad? So it’s a very good asset for us and we’ve made that asset a success not by making concrete change but by avoiding it. Now Burlington Northern itself has been quite clever at adapting technology to their railroad. Imagine the good luck of being able to take an existing railroad and double-decking all of the trains and raising the heights of the tunnels. All of a sudden you have twice the capacity at very little incremental cost which is what that railroads have done.

“Everybody uses new technology but it really helps to have a position [within a business] that can’t be taken away by new technology. How else are you going to carry goods from the port of Los Angeles to Chicago except on a railroad?

“I did not make my fortune, by and large, on the cutting edge of technology.” Because of how quickly it changes and how much it can be disrupted by newer concepts, tech investors must tread carefully. For investors and business operators alike, “Technology is a killer as well as an opportunity.”

“All successful investment involves trying to get into something that is worth more than what you are paying.”

Present-day speculators in high-flying tech companies take heed. The history of overpaying for shares of such companies is loaded with examples where that cutting edge sliced directly into the business of the tech darling du jour, leaving speculators with losses and disappointment.

What is one of your time-tested methods that helped you become successful in business and investing?

“I’ve spent a lifetime trying to avoid my own mental biases. A. I rub my own nose in my mistakes. B. I try to keep things as simple and fundamental as I can. And C. I like the engineering concept of a margin of safety.”

Warren Buffett’s teacher, Ben Graham, applied the margin of safety concept to investing in suggesting that the investor is more likely to succeed if paying a price for shares that is considerably below that which the investor believes them to be worth. Buffett analogized it to building a bridge that can withstand the weight of 30,000-pound trucks but driving only 10,000-pound trucks across it.

Returning to Munger: “I’m a very blocking and tackling kind of thinker. I just try to avoid being stupid. And I have a way of handling a lot of problems: I put them on what I call my ‘too hard pile.’ And then I just leave them there. I’m not trying to succeed in my ‘too hard pile.’”

Still, Charlie is not perfectly immune to the siren song of a good challenge: “Oh, I sometimes get into things that are too hard. And when that happens,” he says bluntly, “I fail.”

Yet the investor simply cannot cower in the corner, too fearful to make a move. One must make mistakes in business and investing: “Of course I’ve made bad business decisions. You can’t live a successful life without doing some difficult things that go wrong. That’s just the nature of the game and you wouldn’t be sufficiently courageous if you tried to avoid every single reverse [in fortune].”

Is it possible to teach people to be great investors?

“I don’t think you can make great investors out of most people. I think great investors to some extent are like great chess players – they’re almost born to be investors. Obviously you have to know a lot but partly it’s temperament. Partly it’s deferred gratification: you’ve got to be willing to wait. Good investing requires a weird combination of patience and aggression and not many people have that. And it also requires a great amount of self-awareness about what you know and what you don’t know. You have to know the own edge of your own competency. And a lot of brilliant people are no good at knowing the edge of their own competency. They think they’re way smarter than they are. Of course that’s dangerous and it causes trouble.

“Obviously it helps to know the basic math of Fermat and Pascal. But anybody with any sense knows that stuff. But having the temperament – where Fermat and Pascal are as much a part of you as your ear and your nose – that’s a different kind of a person. And I think it’s hard to teach that.

— Charlie Munger“What I would say is the single most important thing if you want to avoid a lot of stupid errors is knowing where you’re competent and where you aren’t. And that’s very hard to do because the human mind naturally tries to make you think that you’re way smarter than you are.”

“Warren and I have talked about this. In the early days when we’d talk with others about our way [of investing], which was working so well, we found some people got it and they instantly converted to our way and they did very well. And some people, no matter how carefully we explained it, and no matter how successful they were [in their own field], they could never adapt it. They either got it fast or they didn’t get it at all.”

On the changes in the retail landscape:

“I don’t think [brick and mortar in-person] retail is going to completely go away. It’s been around for thousands of years. But certainly it’s been a very difficult place to make money because of what the internet has done.

“I recently had a friend send me a blue blazer that was bought on the internet from China – and it cost $42 delivered. It may not have been a perfect blazer, but it was an amazing blazer for $42. The person who created that blazer gave some little factory an order for 100,000 of them at once. And those had been pre-sold using the internet. So it’s the most extreme kind of kill-all-your-competitors type of selling I’ve ever seen. Of course traditional retailing hasn’t coped well with something like that. How good is it for Brooks Brothers when someone can deliver something like that over the internet from China for $42? And it didn’t look like too bad of a blazer to me, either. Retailing has just gotten very tough.

“These changes are always good for some investors and bad for others. But when they’re bad, they’re very bad.”

Investors should focus on what can be predicted – not the overall economy:

“I did not make my fortune, such that it is, by making macroeconomic predictions better than other people. What Buffett and I did was we bought things that were promising and sometimes we had a tailwind from the economy and sometimes we had a headwind. And either way, we just kept swimming. That’s our system.”

At Berkshire, Warren and Charlie are “not trying to play the game of getting big advantages out of the big booms and busts… You’re not really trying to predict what the economy will be like 18 months from now.”

Charlie was asked, “Do smarter people predict the future better than others?”

“That’s a very interesting question. You could argue that both ways. A lot of smart people think they’re way smarter than they are; therefore, they do worse than dumb people. [Laughs.] It’s very common to be utterly brilliant and think you’re way smarter than you are. I think Warren and I have been pretty good at avoiding that mistake. We’re pretty modest about our intellect. I know what my mental capacity is. And it’s pretty low compared to the best it could possibly be.”

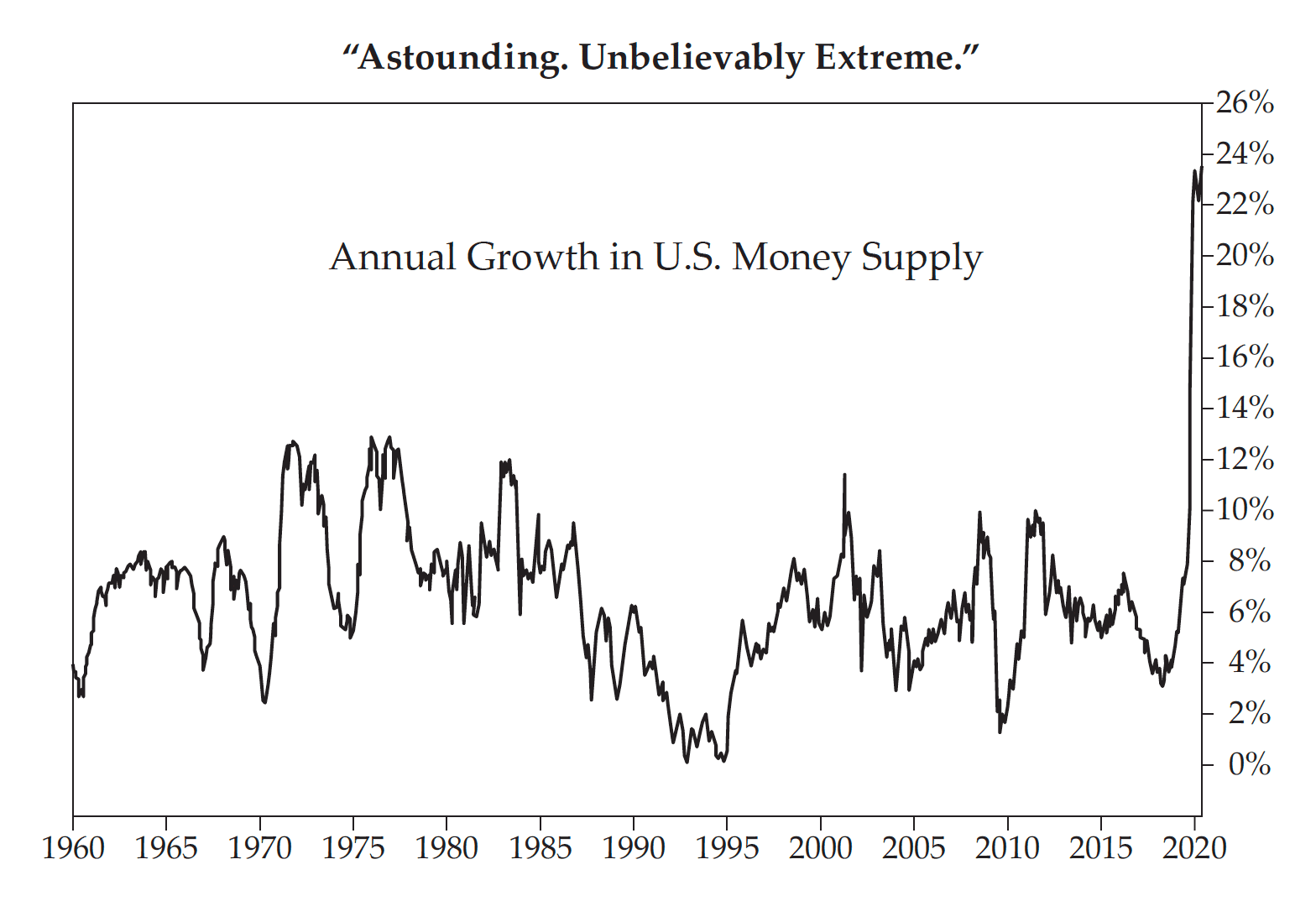

With that, Charlie was asked to make a prediction: where will all the Federal Reserve’s massive stimulus and the U.S. Government’s ballooning fiscal deficits lead us?

“It’s one of the most interesting questions anybody could ask. And we’re in very unchartered waters. Nobody has gotten by with the kind of money printing we’re doing now for a very extended period without some trouble. And I think we’re very near the edge of playing with fire.”

The money supply in the U.S. has exploded higher by 25% in the past year – an unprecedented annual increase.

“Remarkable is not strong enough a word. Astounding would be more like it. It’s unbelievably extreme.”

One fear is that this increase in the domestic money supply will lead to dramatic consumer price inflation.

Low interest rates are causing unusual behavior everywhere:

“Some little European government borrowed money recently for some tiny little fraction of 1% for 100 years! Now that is weird,” says Munger. “What kind of a lunatic would loan money to a European government for 100 years at less than 1%?”

In closing, Charlie was asked what he is most proud of.

“I’m proudest of avoiding some things I don’t like. I don’t like irrationality and I’ve worked to try to avoid it in my life. I haven’t succeeded of course, nobody does, but I’ve done better at that than I thought I would.”

FRED MARKS: IN LOVING MEMORY

It saddens us to deliver the news that on December 25, 2020, 10 days shy of his 88th birthday, Cheviot’s founder and our dear friend, Fred Marks, passed away at his home in McKinleyville, California. His lovely wife, the Honorable Marilyn Miles, was at his side.

Most of us know Fred as the careful value investor who founded and presided over Cheviot for nearly 30 years, but Fred was much more. A life-long learner and ever-curious, Fred was also an accomplished violinist, a yogi (and a lover of Yogi Berra-isms), a teacher, a ballroom dancer, a lawyer, a scholar, a prolific writer, and a voracious reader of subject matters that were impressively wide in range. He could discuss the finer points of classical music, UCLA basketball, and every cubic inch of a car’s engine, switching gears seamlessly between those disparate subjects.

Fred had an enormous vocabulary and would use words that caused us to nod our heads and then retreat quietly to open the dictionary. When we think of Fred, we think of one word he particularly liked: stalwart. Webster defines it as “marked by outstanding strength and vigor of body, mind, or spirit.” It didn’t matter to Fred if a word that he liked, such as stalwart, sounded like something a dermatologist might remove. If it was the right word with the exact meaning that he intended, he used it. That was Fred. Stalwart.

Fred’s knowledge of stock market and economic history was encyclopedic, and he called on this expertise to inform the business and investment decisions that kept Cheviot’s clients’ accounts afloat through turbulent waters and moving forward in tranquil times. But it wasn’t simply Fred’s investing acumen that accounted for his success and the success of Cheviot’s clients. It was also Fred’s unassailable principles of fairness, honesty, transparency and hard work that distinguished Fred and Cheviot from other advisors in what Fred sometimes referred to as the “financial disservices” industry. We have yet to meet anyone in business with greater integrity than Fred.

Always a gentleman, anyone who knew Fred was treated with kindness and respect. He was a caring and thoughtful man who valued his relationships with others. In those relationships, he cherished the opportunities to exchange ideas and learn new things. In the work setting, Fred was equally kind, flourishing as a teacher and role model. He was forever uncomfortable with the term “boss,” and preferred to be called by, and refer to, his employees as “colleague” or “team member.”

It is quite an accomplishment to build a small business from scratch and an even bigger one for it to thrive for decades. Whenever he was asked what his goal was for Cheviot, Fred never spoke of growing the firm to a certain size as so many others do. Instead, he would always reply, “to continue to satisfy our clients and simply to help them.” For those of us who had the daily pleasure of working side-by-side with Fred at Cheviot (as Darren did for 15 years and David for 7), we will forever remember him fondly and with the deepest appreciation for his giving us the opportunity to be part of a very special company. He excelled at modeling the skills and behavior necessary to manage and grow a practice into an enterprise that will flourish for decades to come. We are forever grateful to Fred for being both a wonderful friend and the best boss “colleague” we could have ever wished for.

After his retirement eight years ago, Fred visited us in our offices dozens of times. While his visits came less frequently after his early 2016 move to Northern California, he continued to greet us regularly with thoughtful phone calls and emails (some greater than 2,000 words in length!). Often those missives were about topics other than investing, such as documentaries or books that he thought were worthwhile and educative. Sometimes, unannounced, we would receive books from him in the mail. Just as we think about him regularly, he was always thinking of Cheviot and its clients in a most supportive way.

In the investment world, we often discuss gains and losses. Fred’s passing is a tremendous loss for all that are close to him. But we will hold dear the gains we enjoyed from being near him as we carry on in his honor.

Frederic G. Marks (1933-2020)

Founder: Cheviot Value Management

ABOUT CHEVIOT

Today, Cheviot Value Management is one of the oldest independent investment advisors in Los Angeles. Its founder, Frederic G. Marks, was an experienced business attorney with a bird’s eye view of the struggles his clients faced when investing their hard-earned savings. Repeatedly, he witnessed his clients incurring losses or being mistreated – sometimes without knowing it – by financial services professionals. Since its founding in 1985, Cheviot’s mission is to provide financial peace of mind through careful investing and thoughtful financial advice. Unlike what Fred witnessed elsewhere in the financial services industry for so many years, his goal for Cheviot was to put the interest of the client ahead of all else. Just be helpful.

We begin, in Fred’s words, by helping clients avoid “uninformed speculation under the guise of investment.” Based on the teachings of legendary investors Benjamin Graham, his most famous student Warren Buffett, and his business partner, Charles Munger, Cheviot seeks to own high quality investments for its clients (and members of the firm right alongside them). Our approach aims to produce a more stable growth trajectory, with less volatility than occurs in the stock market. This helps our investors sleep well at night and enjoy greater long-term success.

Cheviot’s Purpose:

We give our clients peace of mind through safety-first investing, long-term growth, and a steady stream of retirement income. Cheviot prides itself on meeting the long-term financial goals established with our clients and on providing attentive and personal service.

Four principles on which Cheviot was founded:

Integrity:

Put the client first in everything we do.

Invest in securities that can be bought or sold quickly and inexpensively.

Flexibility:

There are no lock-up periods; clients may access their funds at all times.

Affordability:

Invest for the long-term, minimizing all costs and taxes.

Why Cheviot?

We have decades of independent and unbiased experience, serving clients since 1985.

We invest for ourselves and our families the same way we invest for our clients: We “eat our own cooking.”

We do not sell any investment “products” nor are we affiliated with any other financial service companies that do. There are no hidden fees.

We have been recognized by the financial industry’s leading publications including, Barron’s, Bloomberg, The Wall Street Journal, Money Magazine, Fox Business, the Business News Network and CNBC.

We maintain well respected credentials in the financial industry, including the Certified Financial Planner (CFP®) designation.

We treat our clients in the way we would desire if our roles were reversed.

CREDITS

Darren C. Pollock, David A. Horvitz, Jim Whiting, and Scott Krisiloff, CFA authored this issue of Investment Values.

DISCLOSURES

Founded in 1985, Cheviot Value Management, LLC specializes in providing investment portfolios with the long-term goals of growth of capital and income production over time. Included within the management of a client’s investments, Cheviot Value Management, LLC also provides financial planning advice including potential strategies related to tax considerations, estate planning, insurance coverages, philanthropy, and next generation preparation. While not a professional tax or legal advisor, Cheviot Value Management, LLC assumes no liability for any tax or legal advice given. Cheviot Value Management, LLC offers such suggestions with the expectation that they will be further examined by a tax or legal professional.