— Ben Graham“Even the intelligent investor is likely to need considerable willpower to keep from following the crowd.”

In this Issue:

- Our Investment Outlook

- The One Thing Newton Could Not Calculate

- Cheviot’s Graphical Interlude

- Credits, Disclosures, & Notes

OUR INVESTMENT OUTLOOK

Have you heard the one about herd behavior? We don’t know this joke’s origin, but we heard Charlie Munger say it: “A teacher asks a class a question: ‘There are ten sheep in a pen. One jumps out. How many are left?’ Everyone but one boy said nine are left. That one boy said none are left. The teacher said, ‘You don’t understand arithmetic,’ and the boy said, ‘You don’t understand sheep.’”

In recent months, pockets of the stock market increasingly played host to stampedes, where share prices quickly ran both higher and lower in bursts of excitement for many newcomers to financial markets. The unusual times of the past year continued into the first quarter of 2021.

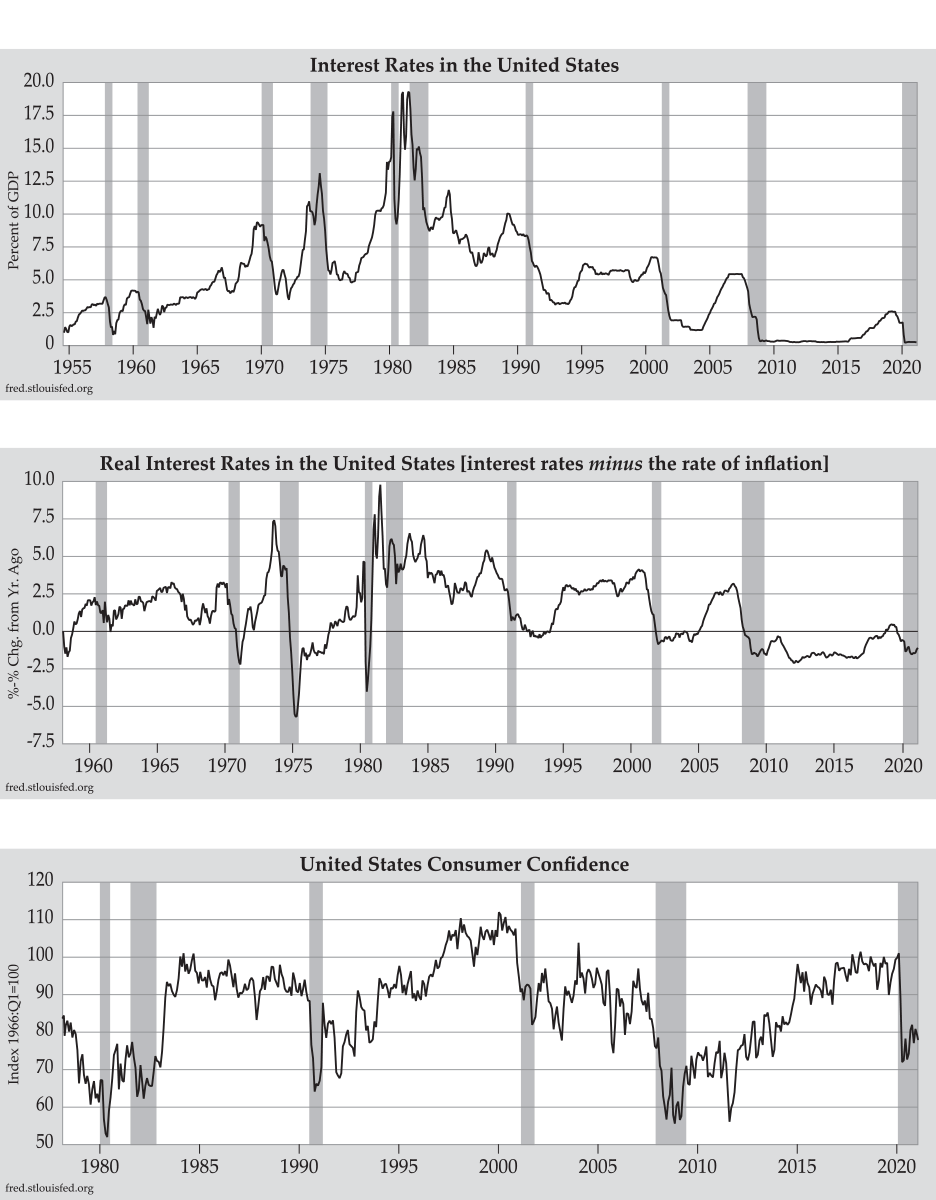

Fortunately, many sectors of the economy are seeing further progress as both vaccines and stimulus checks continue to be distributed to millions of Americans. The U.S. (and global) economy still has a very long way to go toward achieving pre-Covid status and large economic stimulus will remain in force domestically for as long as Congress agrees to keep the spigot running. At the same time, the U.S. Federal Reserve will keep interest rates low and take other extraordinary measures so that financial markets operate with plenty of liquidity.

Those extraordinary measures include the monthly purchase of $120 billion in U.S. Government bonds and mortgage-backed securities (for perspective, this amount – lasting more than a year now – is larger each month than any month during the then record-setting rounds of stimulus which followed the Great Financial Crisis of 2008-09). Additionally, and in the words of Fed Chairman Jay Powell, the Fed “is not thinking about thinking about raising interest rates” – even after the economy begins to heat up.

This pedal-to-the-floor approach by the Fed finally sent shivers up the spine of the bond market last quarter, causing a wave of bond sales – which pushed up interest rates – out of fear that the Fed would allow future inflation to run hotter than is wise. (Future inflation erodes the value of bonds, thus the wave of selling in the bond market.) The late great former Fed Chairman Paul Volcker, canonized in the financial community for his ability to “break the back of inflation” in the early 1980s, in years past was asked about the Fed’s attempts to provoke higher inflation. “Good luck in that,” he replied. “All experience demonstrates that inflation, when fairly and deliberately started, is hard to control and reverse.”

The bond market also may be convinced that massive and ongoing fiscal and monetary stimulus will cause the economy to overheat, forcing the Fed to raise interest rates earlier than it says it will. But can the Fed raise interest rates without causing significant problems throughout the markets and economy? In the fourth quarter of 2018, when the Fed nudged rates higher by one-quarter of one percent for the fourth time that year – pushing them to 2% – widespread panic in financial markets ensued. As we have written in these pages since the Great Financial Crisis of 2008-09, the extreme indebtedness of the U.S. economy, at virtually all levels, causes economic activity to be overly dependent on low interest rates. This creates an economic fragility that becomes exposed when interest rates rise.

The Fed is now in the difficult position of convincing the bond market that it will act responsibly by raising interest rates should inflation percolate. And the Fed will need further fiscal stimulus from the U.S. Government to keep the economic rebound progressing against the likelihood that raising rates to fight inflation may stall the recovery and damage hopes for continued improvements in employment.

Meanwhile in the stock market, mini manias ebb and flow. Excess money from stimulus checks continue to seep into the stock market, fueling speculative behavior in individuals – many of whom should not be gambling in the market. Tens of millions of Americans opened online stock trading accounts in 2020 and 2021.

GameStop, a physical retailer whose sales of video games and consoles have been eroded by online competition, enjoyed a mania in its stock that was so large that participants, including the purported leader of the stock’s rally – a man who goes by the Reddit message board moniker “Roaring Kitty,” were called to testify remotely to members of Congress. (You can’t make this stuff up.) It was estimated that 10% of all Americans bought shares of GameStop in January. Against revenues of $5 billion in 2020 (down steadily from more than $9 billion in 2016), GameStop has not made a profit since 2018. Before the mania engulfed its shares in January, all of the company’s shares were worth less than $400 million. At its late-January peak, the same company’s total market value was 60 times higher, or $24 billion. This value has fallen by nearly half as of March 31st and, despite hopes of a business turnaround, we say caveat emptor.

A good old fashioned stock market mania always invites a horde of new initial public offerings (“IPO”). In little more than the first two months of 2021, more than 302 companies went public – two-thirds of the total number of companies going public throughout all of 2020 (which was itself a strong year for IPOs). In the rush to sell its shares while the public’s appetite for new companies remains strong, the quality of IPOs has sunk to a record low: 81% of IPO’s in 2020 represented businesses that were profitless compared with 73% at the prior peak of IPO excess in the great bubble of 2000.

For genuine investors, corporate profits are the most important long-term driver of stock prices. Shares of a loss-making business represent a speculation that the company will improve its fortunes in the future or that the shares will fluctuate higher on that hope, allowing the speculator to flip his or her shares to another buyer (the latter is called “the greater fool theory” because it requires a greater fool to pay a higher price). Doing so is harder than it sounds and speculations, especially those reaching mania status, usually end badly.

With the hard-earned money that you entrust to us to fund your retirement, to pay for education expenses, and to insure that your charitable foundations can improve the lives of others, we will not speculate. We will continue to execute on our time-proven method of owning the shares of high-quality and highly profitable businesses within a portfolio where the weightings of those holdings are calibrated according to our analysis of each investment’s valuation relative to expected conditions in the economy and financial markets.

We will leave the speculating to others. Like Roaring Kitty. Or Isaac Newton.

THE ONE THING NEWTON COULD NOT CALCULATE

Events of the past year brought countless new participants into the stock market. Though inexperienced, a large number of these individuals are now playing what they believe to be a game that carries decent odds for success. In certain segments of the stock market, this influx of new participants also created small manias which will likely end badly.

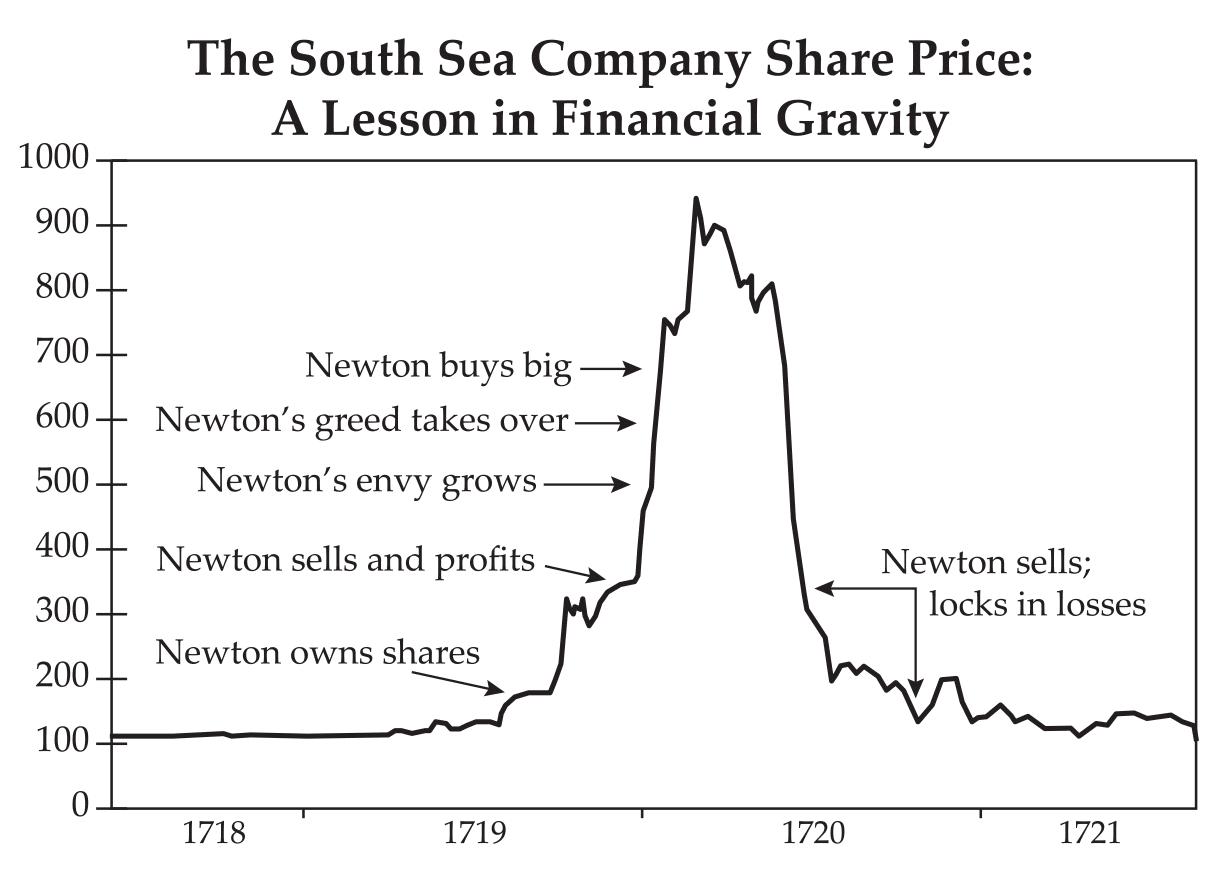

Though not the first financial market debacle of its kind, the boom and bust of Britain’s South Sea Company is the financial event that gave birth to the descriptive term “bubble.” And, despite taking place in 1720, it continues to provide lessons that are instructive for present-day investors.

Before its shares experienced a meteoric rise and catastrophic fall, the South Sea Company was a bumbling shipping company. Then, in 1719 the company secured from the British Parliament a monopoly to trade with colonies in the West Indies and South America belonging to Spain. To repay the government for granting it this monopoly, company shares were issued to holders of British government debt in exchange for their debt, thus removing the obligations of Parliament from private hands. Government debt holders were amenable to this swap since the South Sea Company had a government-issued and protected monopoly that, it would seem, was certain to become very valuable.

In the first half of 1719, shares of the South Sea Company traded hands for 128 British pounds apiece. Through tremendous company-generated promotion, much of which proved later to be false, the share price began to rise. By the end of the year, one South Sea share cost more than 400 British pounds. Using their shares as collateral, large sums of money were lent to South Sea shareholders which then were used to buy more South Sea shares. This recycling of funds produced an upward spiraling of the share price that would reach its peak in March 1720 at close to 1,000 British pounds per share.

The economic backdrop in London at the time was ripe for a financial mania. The newspaper had recently become that period’s version of this era’s internet. New industry generates much enthusiasm and late 1719 through 1720 saw an explosion in speculative initial public offerings (“IPOs”). This speculative mania, like every one that came before and since, ended in disappointment for a large number of its participants.

The bust of 1720 ushered in an era of economic conservatism which stymied the region for decades. As we have witnessed in more recent times, widespread financial losses bring calls for punishment of those executives who presided over the boom and subsequent bust. Proposed levies for the perpetrators of the South Sea mania were severe. One member of the House of Commons believed South Sea directors should be sewn into sacks – along with a snake – and drowned. (To which we ask, why harm the snake?!)

Gravity Exacts a Price

While the bubble was inflating, the general perception was that only a fool would not eagerly invest in shares, including those of the South Sea Company. Sir Isaac Newton was no such fool. During the Great Plague of London (1665-1666), the 22-year-old Newton retreated from Cambridge to his family’s farm to quarantine. During that time, he laid the foundation for a novel type of mathematics later referred to as calculus and set in motion what are now long considered universal truths about inertia and gravity. (Compared to what many of us are doing during quarantine, Newton qualifies as a real show-off.)

As the inventor of calculus, pioneer in physics, expert chemist, and Master of The Royal Mint (producer of England’s currency) for 28 years, Newton was well-equipped with the intellectual tools to understand and steer clear of the irrational boom-and-bust traps of financial markets. But not even someone of his staggering genius could resist the emotional allure of the chance to get rich quickly.

Newton was a shrewd and experienced investor and happened to be a shareholder of the South Sea Company for many years before its explosive lift-off. Having first bought shares in 1713, Newton’s investment managed to produce a satisfactory profit. So, with the share price beginning to rise parabolically in 1720, Newton wisely sold. This was purely rational, a well-executed example of not allowing market volatility to guide the investor but instead to provide the investor with intelligent opportunities to act.

Continued after interlude, below…

Cheviot’s Graphical Interlude

Yet, in the aftermath of his sales as South Sea shares continued to soar in price, Newton was forced to endure something many market participants throughout time have great difficulty with – the pain of watching his friends and neighbors make quick profits. This proved to be Newton’s downfall despite his immensely powerful and otherwise rational mind. Newton’s emotions took control, neutralizing his intellect. He joined the herd, purchasing South Sea shares again – though now at a far higher price – using the majority of his available money, plus borrowed funds, for the acquisition. Similar to the well-recognized combination of “panic then sell,” this was “panic then buy.” Newtonian FOMO.1

Within the same year, the South Sea share price peaked and then quickly fell. Now, hoping to be rid of the shares before they fell any further, Newton sold near the bottom. Succumbing to the emotions of envy and greed, he wound up losing much of his life’s savings. Whereas one could live quite nicely for an entire year on 200 British pounds, Newton’s losses may have approached 100 times that amount (or the equivalent of perhaps as much as 20 million dollars today). Newton, the great thinker whose finances were felled by the siren song of financial markets, later lamented, “I can calculate the motion of the heavenly bodies, but not the madness of people.”

All the more surprising was how someone of his cognitive caliber could fall prey to such irrational behavior. The philosopher Voltaire said Newton otherwise “was never sensible to any passion [and] was not subject to the common frailties of mankind.”

There is just something about the stock market – and watching others appear to make large sums, even if temporary – that can cause wise individuals to lose their rationality.

Though he could never again bear to hear the name “South Sea,” the experience made Newton realize that there was no room for speculation with his life’s savings. From that time forward he took the more cautious road with his personal finances. Before the time of his death seven years later, Newton was again comfortable financially.

Lessons for Investors Today

Invest rationally. Don’t rationalize.

By putting all of his eggs in one basket, Newton believed that buying South Sea shares at a higher price was a sure thing. If he believed that he was being rational, how can we non-geniuses avoid succumbing to a similar fate? One key is recognizing our propensity to replace rationality with rationalizing. The emotions of greed, envy, FOMO, and the comfort of joining the herd are just a few potential disruptions to a rational process. In the abstract, speculating in a company whose shares are in a bubble is understood to be sheer financial madness, but when “easy money” beckons, speculators can find ways to support their decision. These days, the Reddit rallying cry of “sticking it to the suits on Wall Street” also stands out to us as a bad investment motivator.

As Newton proved 300 years ago, staying rational is a difficult task for even the smartest individuals throughout history. In fact, when asked to distill his business and investing success down to just one word, Berkshire Hathaway Vice Chairman Charlie Munger quickly and emphatically replied: “Rational.”

Purchase companies for the long-term.

The stock market can be a casino for gamblers or a place where investors participate in the long-term growth of a business. Owning companies that have the capacity to earn consistently high returns on capital and to grow their earnings slowly but surely over time is usually a safer, albeit at times more boring, path to growth. Warren Buffett likes to acquire shares of companies as if the stock market will be closed for the next ten years. Millions of investors during the mania that exists in pockets of financial markets today are measuring their holding periods in days if not less. Great investors like Buffett are not interested in the buying and selling of shares but in the holding of stable, unexciting – yet continuously profitable – companies. There is no room here for companies like GameStop.

Avoid the exciting.

When it comes to investing, boring is beautiful. And the South Sea Company was anything but boring. It was far more akin to an over-hyped dot-com stock or an Enron with what proved to be fictitious earnings. A lesson still valuable today is to avoid those types of companies, especially so if your friend or neighbor claims to be making a fortune in them. Situations like those are often on the verge of disaster and executing a timely exit is nearly impossible. Such is the way with speculations.

Peter Lynch, a top mutual fund manager during the 1970s and 1980s, once said, “If I could avoid a single stock, it would be the hottest stock in the hottest industry, the one that gets the most favorable publicity, the one that every investor hears about in the carpool or on the commuter train – and succumbing to the social pressure, often buys.” One reason for avoiding these shares is because popular stocks are highly priced relative to their true, underlying value. Over time, those stocks tend to perform poorly.

Lynch did not discover new ways to view the laws of motion, gravity, or various forms of mathematics. But, when it came to investing, he knew what to avoid and how to focus on the long term. 2

ABOUT CHEVIOT

Today, Cheviot Value Management is one of the oldest independent investment advisors in Los Angeles. Its founder, Frederic G. Marks, was an experienced business attorney with a bird’s eye view of the struggles his clients faced when investing their hard-earned savings. Repeatedly, he witnessed his clients incurring losses or being mistreated – sometimes without knowing it – by financial services professionals. Since its founding in 1985, Cheviot’s mission is to provide financial peace of mind through careful investing and thoughtful financial advice. Unlike what Fred witnessed elsewhere in the financial services industry for so many years, his goal for Cheviot was to put the interest of the client ahead of all else. Just be helpful.

We begin, in Fred’s words, by helping clients avoid “uninformed speculation under the guise of investment.” Based on the teachings of legendary investors Benjamin Graham, his most famous student Warren Buffett, and his business partner, Charles Munger, Cheviot seeks to own high quality investments for its clients (and members of the firm right alongside them). Our approach aims to produce a more stable growth trajectory, with less volatility than occurs in the stock market. This helps our investors sleep well at night and enjoy greater long-term success.

Cheviot’s Purpose:

We give our clients peace of mind through safety-first investing, long-term growth, and a steady stream of retirement income. Cheviot prides itself on meeting the long-term financial goals established with our clients and on providing attentive and personal service.

Four principles on which Cheviot was founded:

Integrity:

Put the client first in everything we do.

Invest in securities that can be bought or sold quickly and inexpensively.

Flexibility:

There are no lock-up periods; clients may access their funds at all times.

Affordability:

Invest for the long-term, minimizing all costs and taxes.

Why Cheviot?

We have decades of independent and unbiased experience, serving clients since 1985.

We invest for ourselves and our families the same way we invest for our clients: We “eat our own cooking.”

We do not sell any investment “products” nor are we affiliated with any other financial service companies that do. There are no hidden fees.

We have been recognized by the financial industry’s leading publications including, Barron’s, Bloomberg, The Wall Street Journal, Money Magazine, Fox Business, the Business News Network and CNBC.

We maintain well respected credentials in the financial industry, including the Certified Financial Planner (CFP®) designation.

We treat our clients in the way we would desire if our roles were reversed.

CREDITS

Darren C. Pollock, David A. Horvitz, Jim Whiting, and Scott Krisiloff, CFA authored this issue of Investment Values.

DISCLOSURES

Founded in 1985, Cheviot Value Management, LLC specializes in providing investment portfolios with the long-term goals of growth of capital and income production over time. Included within the management of a client’s investments, Cheviot Value Management, LLC also provides financial planning advice including potential strategies related to tax considerations, estate planning, insurance coverages, philanthropy, and next generation preparation. While not a professional tax or legal advisor, Cheviot Value Management, LLC assumes no liability for any tax or legal advice given. Cheviot Value Management, LLC offers such suggestions with the expectation that they will be further examined by a tax or legal professional.

NOTES

- “Fear of Missing Out” is perhaps the least known but most human of Newton’s accomplishments. ↩

- Peter Lynch is one famous investor who successfully resisted the type of market temptations to which Newton fell victim. We use Lynch as an example here perhaps in part because he was born in Newton, Massachusetts.↩