— Charles Dow“To know values is to know the meaning of the market.”

In this Issue:

HAPPY BIRTHDAY, DOW JONES: WHAT A 125-YEAR-OLD INDEX CAN TEACH US ABOUT INVESTING

We like birthdays. And when the Dow Jones Industrial Average (“the Dow”) turned 125 years old this past May, we noticed that it resembled a spring chicken compared to the lengths of other financial lives. The Dow’s lifetime, for example, is a far cry from the several thousand years of gold being used as a store of value and medium of exchange, or the world’s earliest coin registering well over 2,000 years old, or even the first stock exchange dating back more than 400 years ago. But relative to cryptocurrencies, most of which have existed for just a few short years, or non-fungible tokens (“NFTs”), which are as new as they are mysterious (and of which we are skeptical), the Dow seems closer to an ancient relic. Yet the Dow’s rich history, its quirks, and the lessons offered, are often overshadowed by investors too focused on its daily fluctuations.

To many, a 300-point move in the Dow is attention-grabbing. After all, 300 Dow points is nearly eight times the entire value of the Dow when it began in 1896. It is also more than half the points lost on the day stocks crashed in 1987. And while 300 points sounds like a lot when heard on the nightly news, it amounts to less than a one percent change given the current value of the Dow. 300 points today simply is a non-event, much a-Dow about nothing. (Forgive us, we couldn’t resist!) Placing the Dow’s point swings in context and understanding the evolution of the index is more meaningful. Investors today can learn much from studying the Dow’s strengths — and weaknesses — as a bellwether.

Before 300-point fluctuations were ever imagined, the Buttonwood Agreement, signed by 24 stockbrokers in 1792, formalized the trading of company shares which had been taking place under a buttonwood tree on Wall Street, in New York City. Today, outside of the New York Stock Exchange, a small buttonwood tree (now more commonly referred to as a sycamore) marks the spot where the earliest stock trading is said to have occurred. It was not until 1884 that a stock market index was created to represent the daily price changes of a group of American stocks. This basket of company shares, the Dow Jones Transportation Index, to this day still contains the shares of 20 transportation companies. It was later unseated as the dominant U.S. stock market index by the Dow Jones Industrial Average.

Charles Dow was a business researcher and writer who, with his statistician colleague Edwin Jones, founded the aforementioned eponymous indices. (Dow was an accomplished fellow who also co-founded The Wall Street Journal.) As opposed to transportation businesses, the Dow sought to represent industrial corporations — the leading American companies of their day — and the daily fluctuations in those share prices. Despite being comprised of only 30 companies, over time the Dow still represents fairly well – though not perfectly and certainly not on a daily basis – the direction of the U.S. stock market as a whole.

How does such a small group of 30 stocks roughly track the movements of the U.S. stock market writ large? To begin, the Dow, like other stock market indices, periodically changes its constituents. The nearby list of the original 12 Dow components portrays a vastly different U.S. economy. None of the Dow’s original holdings remains in the index today. The longest tenured company, Proctor & Gamble, became a member in 1932 at the depth of the Great Depression. With its 1976 inclusion, the 3M Company is the second longest tenured. Nearly half of the Dow components were added in the last 20 years. Just as large businesses must each adapt to stay relevant in their particular industries, periodic replacements within the Dow help keep the index representative of the overall U.S. stock market.

“Are You In or Out?”

For a company to be added to the Dow, it must first be a component of the broader S&P 500 index. Then, the requirements are qualitative, not quantitative. Per the Dow’s selection committee, “a stock is typically added only if the company has an excellent reputation, demonstrates sustained growth, and is of interest to a large number of investors.” Dow adjustments are made “on an as-needed basis.”

When constructing the Dow, another consideration is the price of the stock of the potential addition. A company will not be added if its share price is more than ten times greater than the lowest share price of an existing Dow member. And if a current component’s share price falls below that one-tenth threshold, it will suddenly be at risk of removal. (Once joining the Dow, members are probably less likely to split their shares — unless they grow to too high a figure.) Pfizer was removed in August 2020 because its share price had less than one-tenth the impact on the Dow as the shares of the highest priced companies at that time.

The Dow’s inclusion criteria are highly subjective, much like an individual investor’s portfolio decisions. This should be no surprise since the Dow’s selection committee (as is true of many other indices) is subject to the same behavioral biases affecting all investors. When industries are thriving — or, as stated by the Dow’s pickers, are “of interest to a large number of investors”— the urge is to buy the shares of the most popular companies in that field. This is true even after the price has experienced a significant increase.

The latter half of the 1990s saw a boom in the share prices of tech companies as the internet was being built. All things tech soared in price and, several years into the mania, a pair of thriving tech giants, Intel and Microsoft, were added to the Dow. This occurred during the largest stock bubble in U.S. history and mere months before its peak. The nearby graph shows Intel’s meteoric rise during the tech bubble and when it was added to the Dow at roughly $40 per share. After a final burst higher, the shares then fell by more than half and ten years later were still 50% lower than when they were selected for inclusion.

When the Dow last made changes to the index in late August 2020, the mania for electric vehicles was at its peak. The flip side of that coin saw oil companies as unloved as they have ever been. Consequently, ExxonMobil, a Dow component for 92 years, was removed from the index. In the summer of 2020, ExxonMobil’s shares at $40 were priced full of fear. Today, with less fear throughout the industry and a greater understanding that the transition away from fossil fuels will take a long time, the share price is nearly 60% higher. (See graph below.)

Intel was added 22 years ago, when it was one of the world’s most popular companies, and ExxonMobil was removed last year when it was one of the world’s most unloved companies. At each time, the price was, coincidentally, around $40 and recently, after 22 years for Intel and less than one year for ExxonMobil, both share prices are near $60. Intel’s rate of return on the share price alone for those 22 years is less than 2% per year. This is what happens when an investor succumbs to a good story, ignores valuation and is willing to buy at any level. As Warren Buffett once said, “You pay a high price for a cheery consensus.” And paying high prices usually delivers disappointing if not disastrous results. (See graph below.)

Conversely, with companies where the consensus is dour, the investor may be getting a good bargain. Not only have those who bought ExxonMobil from the Dow sellers received a nearly 60% capital gain, but they also locked in close to a 9% annual dividend yield. To quote Baron Rothschild, “Buy when there’s blood in the streets, even if the blood is your own.”

This is not to say that all additions to and removals from the Dow are ill-timed — far from it. But news of a Dow addition or removal should not be viewed by individual investors as an endorsement or repudiation of the investment merits of that stock at that time.

Continued after interlude, below…

Cheviot’s Graphical Interlude

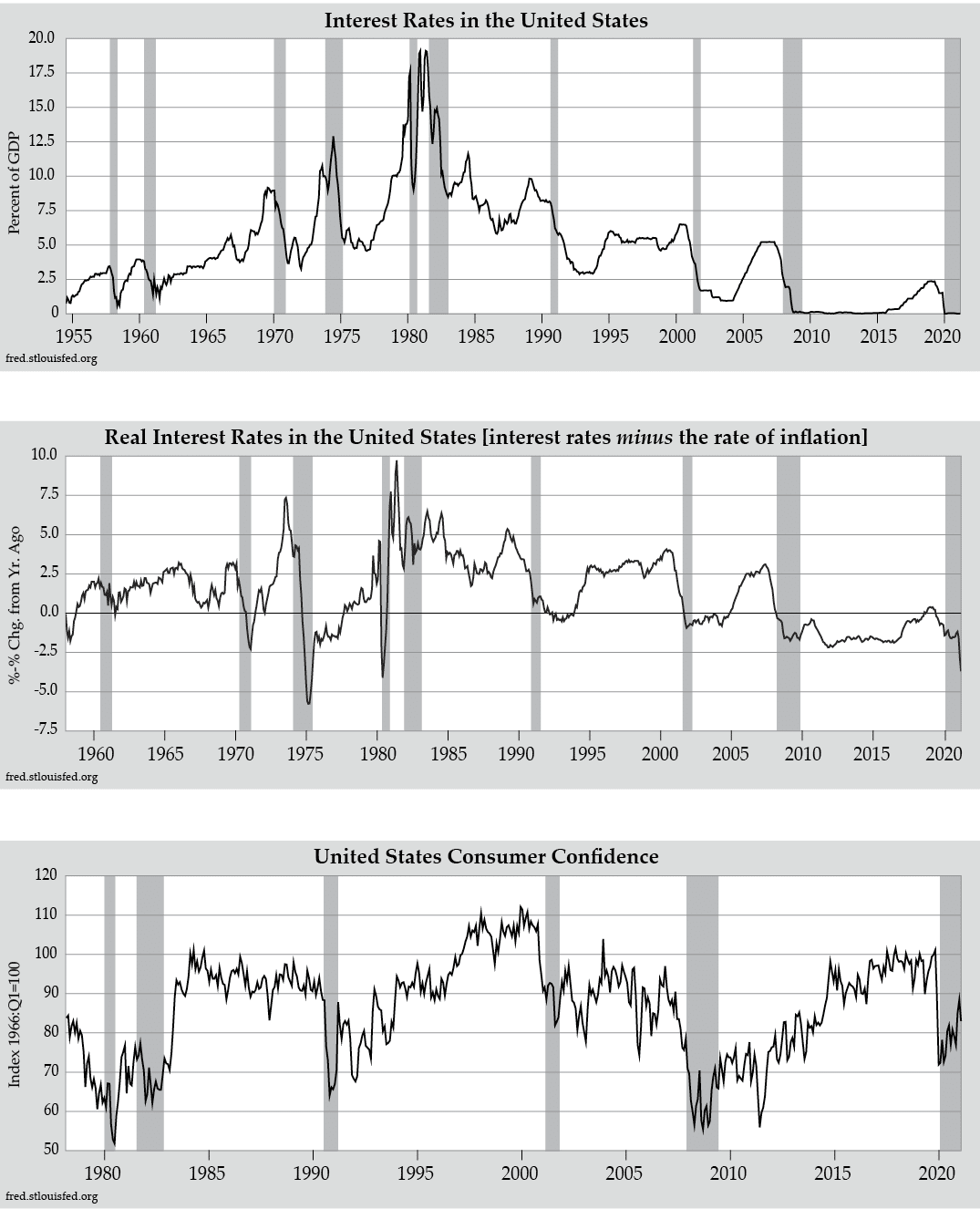

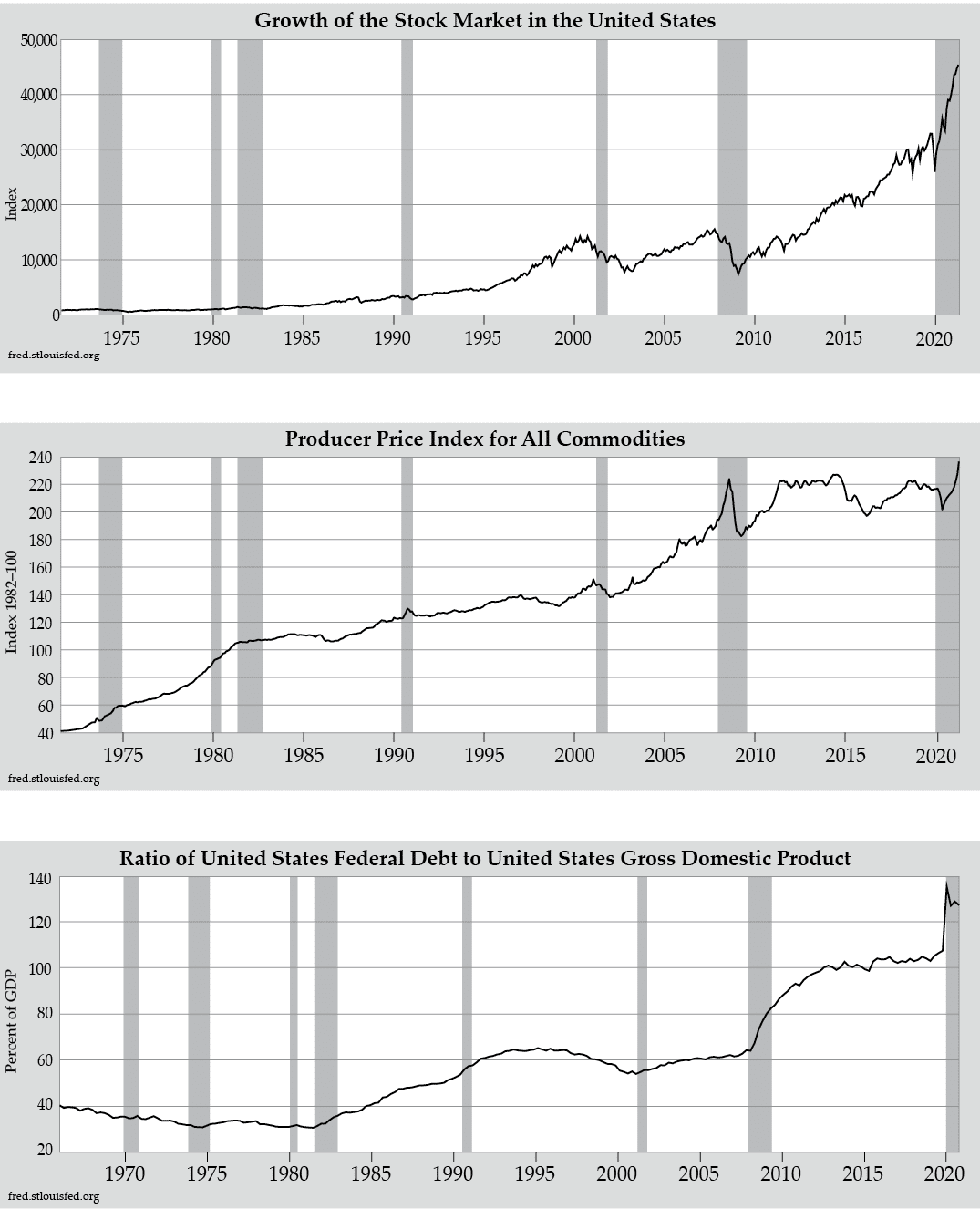

We share a small sample of graphs that we believe paint a broad picture of U.S. economic activity and sentiment. Graph 1, Interest Rates in the U.S., illustrates the peaks and valleys of short-term interest rates over time. Graph 2, Real Interest Rates in the U.S., depicts the level of short-term interest rates adjusted for (or after) inflation. Graph 3, United States Consumer Sentiment, measures the level of confidence American consumers have toward making near-term expenditures. Graph 4, Growth of the Stock Market in the U.S., portrays the long-term increase in U.S. stock prices and often reflects sentiment toward the economy. Graph 5, Producer Price Index for All Commodities, shows the long-term march higher and periodic setbacks in price for a compilation of various commodities used throughout the U.S. and the world. Graph 6, Ratio of U.S. Federal Debt to U.S. Gross Domestic Product, describes the level of U.S. Government debt relative to the size of the U.S. economy.

Though a company’s share price is of great importance to the Dow selection committee, share price alone is not a worthwhile indicator of that company’s value. Just as a stock split does not affect the actual economics of the ownership of those shares (would you rather have one share priced at $50 or two shares priced at $25?), a high or low share price should not matter to individual investors. Yogi Berra may have put it best when he asked for a pizza cut into six slices rather than eight, claiming he didn’t think he could eat eight pieces. But the Dow is a price-weighted index, meaning that a company whose shares are priced higher have a greater impact on the overall movement of the Dow than a company whose shares are priced lower. Does this make sense? Probably not. Would you remove a company from your personal investment portfolio because its price was below an arbitrary ratio relative to another stock in your portfolio with a higher share price? Of course not. Other indices are market capitalization weighted such that the total value of all of a company’s shares is what determines that company’s place in the index’s pecking order. This makes more sense.

Maybe, you might be wondering, it would make even more sense if the amount of a company’s revenues or profits or the value of its assets were what determined where that company ranked in terms of its impact on the index. Doing so might cause the index to more accurately reflect the underlying economy in which the index is domiciled. This concept, called fundamental indexing, exists but it is not how any of the world’s major indices are calculated. (Another concept, equal weighting, says that each component of the index impacts the index identically, thus the largest and smallest company have similar sway. This is a version of indexing that essentially admits not to know how the components should be weighted, so each one is weighted equally.)

Currently, the companies in the Dow with the greatest impact on the index’s direction are UnitedHealth ($401.44 per share as of June 30th), Goldman Sachs ($379.53), and Home Depot ($318.89). The companies with the least sway over the direction of the Dow, due to their share prices being the lowest, include Cisco, Coke, and Walgreens. Remember, a lower share price does not necessarily mean a smaller market capitalization (which equals the price of each share multiplied by all of the shares outstanding). Cisco proves this with a share price that’s one-seventh the price of Goldman Sachs but a total market value that is $100 billion greater.

To gain admission in the Dow, Apple split its shares which lowered the price per share into an acceptable range for the Dow selection committee. And, even though Apple has the largest market cap in the Dow, its weighting ranks it 22nd out of the Dow’s 30 companies (this would have been higher had it split its shares two or three for one instead of seven for one). Microsoft has the second largest market cap and is weighted fourth in the Dow behind the aforementioned UnitedHealth, Goldman Sachs, and Home Depot. The combined market cap of those three businesses is less than half of Microsoft’s $2 trillion.

The big three of UnitedHealth, Goldman Sachs, and Home Depot account for nearly 20% of the Dow’s movements. As an individual investor, if 20% of your portfolio is not invested in those three businesses, it is very unlikely for your portfolio’s daily fluctuations to mimic the Dow’s fluctuations. Furthermore, individual investors are not likely to – nor should they – be 100% invested in stocks and, if they are so aggressive, it is even less likely that their portfolio will be correlated with the Dow. When one sees point swings in the Dow large or small, up or down, they should not expect to see a very similar movement in their own portfolio.

The Dow is an interesting stock market index with a rich history. But, for all its changes and calculation method that reflects the pre-computer era in which it was created, it, like most stock indices, is not worthy of the daily obsession given to it by many market participants. We believe the Dow, again like most indices, could be ignored completely over weeks, months, and even quarters but that is due to our strict long-term investment focus. And that is one thing that we have in common with the Dow: when a company is added to our portfolio, as with the Dow, it is quite possible that it will be held for a considerable period of time. This is because, as odd as it seems and as counterintuitive as it may be to one’s thinking about normal life, in investing it is actually far easier to control the long term than it is the short run.

ABOUT CHEVIOT

Today, Cheviot Value Management is one of the oldest independent investment advisors in Los Angeles. Its founder, Frederic G. Marks, was an experienced business attorney with a bird’s eye view of the struggles his clients faced when investing their hard-earned savings. Repeatedly, he witnessed his clients incurring losses or being mistreated – sometimes without knowing it – by financial services professionals. Since its founding in 1985, Cheviot’s mission is to provide financial peace of mind through careful investing and thoughtful financial advice. Unlike what Fred witnessed elsewhere in the financial services industry for so many years, his goal for Cheviot was to put the interest of the client ahead of all else. Just be helpful.

We begin, in Fred’s words, by helping clients avoid “uninformed speculation under the guise of investment.” Based on the teachings of legendary investors Benjamin Graham, his most famous student Warren Buffett, and his business partner, Charles Munger, Cheviot seeks to own high quality investments for its clients (and members of the firm right alongside them). Our approach aims to produce a more stable growth trajectory, with less volatility than occurs in the stock market. This helps our investors sleep well at night and enjoy greater long-term success.

Cheviot’s Purpose:

We give our clients peace of mind through safety-first investing, long-term growth, and a steady stream of retirement income. Cheviot prides itself on meeting the long-term financial goals established with our clients and on providing attentive and personal service.

Four principles on which Cheviot was founded:

Integrity:

Put the client first in everything we do.

Invest in securities that can be bought or sold quickly and inexpensively.

Flexibility:

There are no lock-up periods; clients may access their funds at all times.

Affordability:

Invest for the long-term, minimizing all costs and taxes.

Why Cheviot?

We have decades of independent and unbiased experience, serving clients since 1985.

We invest for ourselves and our families the same way we invest for our clients: We “eat our own cooking.”

We do not sell any investment “products” nor are we affiliated with any other financial service companies that do. There are no hidden fees.

We have been recognized by the financial industry’s leading publications including, Barron’s, Bloomberg, The Wall Street Journal, Money Magazine, Fox Business, the Business News Network and CNBC.

We maintain well respected credentials in the financial industry, including the Certified Financial Planner (CFP®) designation.

We treat our clients in the way we would desire if our roles were reversed.

CREDITS

Darren C. Pollock, David A. Horvitz, Jim Whiting, and Scott Krisiloff, CFA authored this issue of Investment Values.

DISCLOSURES

Founded in 1985, Cheviot Value Management, LLC specializes in providing investment portfolios with the long-term goals of growth of capital and income production over time. Included within the management of a client’s investments, Cheviot Value Management, LLC also provides financial planning advice including potential strategies related to tax considerations, estate planning, insurance coverages, philanthropy, and next generation preparation. While not a professional tax or legal advisor, Cheviot Value Management, LLC assumes no liability for any tax or legal advice given. Cheviot Value Management, LLC offers such suggestions with the expectation that they will be further examined by a tax or legal professional.